Martin Thomas (MT): I can see four main sorts of possible outcomes to be considered from Trump’s economic jousting.

One: it may reshape some deals, like NAFTA [the North American Free Trade Agreement] to the USA’s advantage or imagined advantage, but after a flurry relations in the world markets will settle down much as before.

Two: By generally shaking up trade relations, and putting pressure on some of China’s protectionist policies, economic life around the world may settle after the jousting into a more “globalized” form, more subject to world-market rules.

Three: The jousting leaves a world-market system operating in much the same way as now, but with the USA now a rogue state on the edge of it rather than the pivotal state in the system. Maybe the system is organized around a new pivot, maybe China.

Four: The jousting begins a serious unravelling of the world-market order, a contraction of supply chains, a re-raising of trade barriers, a push to economic nationalism. The shift is moderate and limited for now, but escalates in the next big economic crisis.

Some articles in the new Socialist Register argue cogently that the third option is not a real possibility. What do you think about the others? And does this list map out accurately the possibilities we should consider?

Leo Panitch (LP): The list is about right. The main question, though, is: will the effects of Trump’s regime, not just his antics at an international level but his presidency itself, be to render the key American state institutions that have been responsible for firefighting financial crises incapable of being effective firefighters.

MT: Yes. As you argue in your book with Sam Gindin, The Making of Global Capitalism, the current world market order has not just evolved automatically: it has been made and managed by the U.S. state…

LP: The U.S. is already acting as a rogue state under Trump. But the system is so dependent on the role of the U.S. state within it, and the American economy, and the American dollar, so that it is difficult to see how the system can dispense with the centrality of the United States.

If Trump’s effects are longstanding, we may face a very dysfunctional system, but one that is not open to reorganization.

In that framework, and with the rise of right-wing xenophobic nationalisms, with some added militarist dimensions, I fear that this could lead to conditions of extreme nationalisms facing off against each other.

The limiting aspect is the degree of integration of the world bourgeoisies with one another. The kind of shift that the Ruhr industrialists [in Germany] undertook between 1928 and 1932 to back the Nazis is hard to see as on the cards given the degree of capitalist integration. That’s where the cloudy crystal ball leaves us.

MT: The centrality of the U.S. in managing the world economic order has not diminished, despite the 2008 crash and despite the fiasco of U.S. policy in Iraq. China’s holdings of Treasury paper are bigger than they were, not smaller. The dollar’s role in world trade has increased, not diminished.

LP: Yes, 88 per cent of transactions are now conducted through the dollar.

MT: At the time of the invasion of Iraq in 2003, a common theory about it was that the USA was doing it in order to head off the euro taking over from the dollar at the centre of world trade.

LP: There were, possibly, policy-makers in the United States who thought that way. There were certainly loads of left-wing commentators who explained it that way. Neither group had much purchase on reality. As we see with Trump, sometimes U.S. policies are undertaken for reasons which are delusional. But most of the arguments inside the Bush administration were, I think, opportunist, of a militarist kind, or about re-establishing the supremacy of the executive vis-à-vis Congress.

Why the argument about the euro becoming the vehicle currency for Iraqi oil sales leading to its replacing the dollar as the world currency was other-worldly… even if you sold oil in euros, those could be exchanged in milliseconds for dollars. Insofar as big capitalists, institutional funds, corporations and so on find the dollar more useful, it is for a multitude of specific reasons to each of them. The dollar doesn’t hang there in mid-air. Its role is embedded in a set of institutions and practices and skills and knowledge which capitalists pay one another for.

The centrality of the City of London in changing the world’s currencies into dollars through derivatives markets and so on is deeply embedded in the institutions of the City of London, including the American banks operating there and the capitalist skills and knowledge built over centuries of British merchant banking. There is no other set of institutions now capable of replacing them. And that’s why, although there will be some marginal movements of jobs from the City of London, even the Bank of England’s most recent warnings about the effects of Brexit do not talk about the City of London being displaced from the role it plays in the dollar markets of the world.

In this very dysfunctional world, affected by Trump’s ascension to the presidency, it is remarkable that the dollar continues to have its centrality. That’s partly because the American economy has done relatively well, compared to others, in the decade since the fourth great crisis of capitalism, but it is also to do with the centrality of the institutions which sustain the dollar in the quotidian workings of global capitalism. But in the end it is because of capitalists’ confidence in the American state as the ultimate guarantor of property and value and wealth and capital, that the dollar remains so central.

MT: In your Socialist Register article with Sam Gindin (“Trumping the Empire”), you refer to the possibility of the central banks becoming the saviour of the existing order.

LP: This is a great irony. The motivation that drove making central banks independent from elected governments, especially in the era of globalization over the last 30 or 40 years, with the IMF virtually dictating to states that central banks must be made independent, was precisely to remove them from democratic pressures.

Above all, the motivation was the fear that working people, as voters, would opt for monetary policies that would provide room for wage increases – that would open the inflationary space that governments have been guarding against since they defeated trade unions in the 1970s and early 1980s.

Now these right-wing patriotic scoundrels who are being elected find that they can’t force the central banks to do their bidding so easily – above all Trump, and in relation to the Federal Reserve.

That really matters. There is plenty of evidence that the Treasury is being severely hampered by the Trump administration in the role it can play as a firefighter and as a functional actor in the global system.

You see that in the G20 meeting in Argentina [30 November and 1 December]. The G20 is essentially a creation of the United States Treasury, which always wrote the communiqués that were then signed by the finance ministers or by the heads of state. Now its is the senior officials of the other finance ministries who have to scramble to produce consensual texts, and the G20 can’t get the U.S. to sign on to them.

Just recently the Financial Times commented on the appointment of Randal Quarles to head the world Financial Stability Board. Quarles has been a long-time senior figure in the Federal Reserve, a smart functionary of the reproduction of capitalist social relations at a global level. The FSB, created in the wake of the 2008 crisis, was headed by Mark Carney [governor of the Bank of England] before him, and before that by Mario Draghi [chief of the European Central Bank]. The appointment of Quarles indicates that the Fed is putting a lot of resources into infrastructure which will keep the links between the European Central Bank, the Bank of England, and the Federal Reserve of a kind that will allow them to do the super-intendence over the transfers of dollars between the central banks and the general sort of coordination and firefighting that was done after 2008. That would indicate that the system is not quite as dysfunctional as it appears to be.

MT: You’ve discussed the possibility that the end-effect of Trump’s jousting will be to open up the Chinese economy more to world markets.

LP: Ever since Trump was elected, you’ve seen the Chinese, especially Xi, plugging the theme that the United States needs to live up to its global responsibilities.

China is the capitalist late-developer which has relied most in the whole history of capitalist development on foreign direct investment. In our essay in the new Socialist Register, Gindin and I quote Xi saying this earlier this year to a group of visiting foreign capitalists that they are going to remove some of their restrictions on foreign capital becoming majority owners of Chinese firms and on foreign financial institutions operating in China.

Removing those restrictions on foreign financial institutions has long been a main goal of Wall Street and previous American administrations – to allow a larger role in China for Goldman Sachs and the rest of them. The Chinese have also signalled that they will not be protecting as much their rights to technology transfer when firms invest in China. So Xi is prepared to move quite a distance. There are internal pressures from many Chinese capitalists themselves, who want a loosening of China’s capital controls.

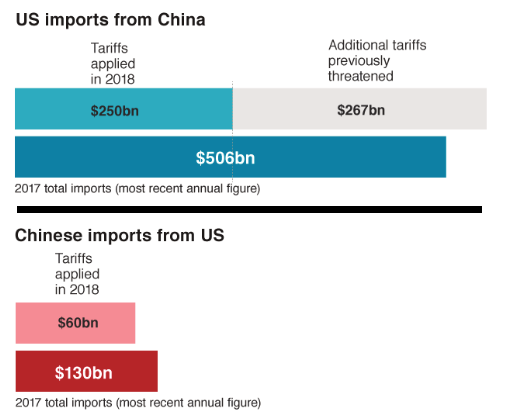

The Chinese are very much the takers of this trade war. They are responding, to be sure, in ways which are designed to inflict some harm on, for example, American farmers producing soy which is exported to China, and are having some effects on U.S. construction companies who rely on Chinese wood products. But the Chinese are not leading this trade war. They are trying to find ways to mollify Trump. All this suggests to me that it is possible that Trump will get his way.

At the same time, the Chinese Communist-capitalists are also nationalists. All of the great Third World Communist-revolutionary movements were in very good part nationalist movements.

How far they can be pushed is a significant question. If you read the essays by Lin Chun and Sean Starrs in Socialist Register 2019, the heavy dose of nationalism that defines the ideology of this Chinese leadership, and especially Xi, may mean that they can’t be pushed too far.

On 1 December, Canadian authorities, at the demand of the U.S. seeking her extradition, arrested Meng Wanzhou, chief financial officer of Huawei and daughter of the founder, someone who has been described as a member of Chinese corporate royalty, on the grounds that her firm has allegedly been involved in breaching American sanctions against Iran. This has produced a furore in China. These things can get out of hand.

It would be misleading, when we look at the structural conditions that put limits on the whole system falling apart, to think that these contingent things can’t have effect. We need to watch this closely. It is not only people of our political orientation who are watching Washington with bated breath.

American capitalists, and the world’s capitalists, are watching with bated breath.

MT: It’s said that the economic jousting between the USA and China isn’t fundamentally about tariffs and trade; it’s about technology transfer and the U.S. wanting to maintain its technological lead.

LP: That’s an important dimension. A lot is done in the U.S., for example on microchips, to limit the Chinese to being assemblers. The Chinese have a very explicit goal of becoming, by the 2030s, fully adept in the technologies themselves. It is clearly a concern of the Americans.

The technology transfer issue has long-term economic dimensions to it, but it also has military-strategic-intelligence dimensions. It does reflect – some of the kinds of behaviour and motivations that defined the old inter-imperial rivalries. Some of it has to do with the capacities of rival military and security apparatuses. The fact that China and Russia are not in NATO and are not in the global intelligence and security establishment that operates under the rubric of the United States. The so-called “five eyes,” Anglo-American countries (USA, UK, Canada, Australia, New Zealand), are at the core of that establishment. The key historical determinant even of Clinton’s and Blair’s view of the world was that Russia and China were not subjected to postwar state reconstruction by American military occupation as Japan and Western Europe were.

MT: The new Socialist Register has material expressing a sceptical view on the prospects of the Belt and Road Initiative [Chinese-sponsored infrastructure development and investment in a range of countries, launched since 2013, to develop a new China-centred trade network].

LP: Yes, I think, we have to take the evidence on this in the outstanding essays by Sean Starrs and Lin Chun very seriously. They show very clearly not only the economic contradictions which have emerged with the Belt and Road Initiative, but also the extent to which China is seen by many other states in southeast Asia in the light of a an imperial power posing the main threat to their national sovereignty.

This is what most people overlook when they see China as forming Asia as a whole into a regional counter-power to the USA, and especially in south-east Asia, China is seen by other nationalist forces as their main enemy. That dimension is largely overlooked when people speak of a multipolar world in which China dominates Asia. As well as the economic limits of the Belt and Road Initiative, there is a very important historical, cultural-nationalist-imperial dimension.

MT: World capitalism is much more integrated in the late 20s and early 30s, and you mentioned that when saying that it is hard to think of the bourgeoisie in any country swinging behind ultra-nationalist forces as heavy industry in Germany swung behind the Nazis.

But there’s another variant historically. In the period up to World War One, people like Bernstein would argue that the degree of integration of capital across borders was such as to make war less and less likely. Writers like Trotsky responded that it was an integration which tended to set up large rival alliances.

The world order became one, not just of molecular struggles between states, but of jousting between large rival alliances. That created the conditions for World War One.

There was a lot of talk in the early 90s about world capitalism developing into three great regional blocs, one dominated by the U.S., one dominated by the EU, and one dominated by Japan. It was mistaken.

What you’ve said about China is an argument against reviving that regional-bloc thesis today. Does that mean the thesis is pretty much ruled out?

LP: Who knows? Karl Kautsky (1854 – 1938) around World War One saw a ruling-class condominium developing among the big capitalist states, along the lines of the Paris discussions which led to the Treaty of Versailles. It didn’t turn out to be all that stable, did it? The flaw in Kautsky’s understanding was that he saw it as a matter of coordination among ruling classes who were accumulating still within the boundaries of their own states or territorial empires. But especially in the second half of the 20th century there was an interpenetration of capital around the world – the material, structural underpinning to the trade and investment agreements made by governments.

It became a different world than that of World War One.

The question we began discussing today was whether the political effects of the current Trump administration will be so dysfunctional as to get in the way of the reproduction of the integration. This is so important to analyse precisely because the economic integration has also produced contradictions, which are increasingly severe in the 21st century. These contradictions partly have to do with the crisis-prone nature of the very volatile global financial system which is essential to tying together global production. They also have to do with the domestic consequences, in class terms, of the ever-greater inequalities of power, income, and wealth which this integrated capitalism produces as states compete to get capital landing inside of them.

Insofar as the world we are living in is increasingly prone to severe contradictions, extending beyond the two I have mentioned to all kinds of morbid symptoms ranging from the climate crisis to the migration crisis and the xenophobia that attends it, we need to see those symptoms as opening up possibilities in terms of revolutionary transformations within particular states which would then have international implications.

But, at the same time, given the weaknesses of the left and of the working classes, those transformations are not going to be triggered by the type of events we’ve seen in Paris [with the “gilets jaunes”], that is, another round of inflammatory protest movements. Since the 1930s, some Trotskyist analysis has been premised on the notion that capitalism is over-ripe for revolution… and thus its fall can be triggered by unexpected conflagrations of any type, which will then have international effects like a falling row of dominoes. I am not of the view that capitalism is, in its material base, “over-ripe for revolution.”

MT: I agree. I know that idea has become a common theme in would-be Trotskyist literature, but I think it comes more from Third Period Stalinism.

LP: So it does.

*

Note to readers: please click the share buttons below. Forward this article to your email lists. Crosspost on your blog site, internet forums. etc.

This article was originally published on Workers’ Liberty.

Leo Panitch is emeritus professor of political science at York University, co-editor (with Greg Albo) of the Socialist Register and author (with Sam Gindin) of The Making of Global Capitalism (Verso).

Images in this article are from The Bullet unless otherwise stated