|

‘We are triply exploited: We are taxed on wages, alienated from wealth created (profits) and we pay interest on the money borrowed from the wealthy to pay for the capital and current expenditure needed for the maintenance of society.’ [1]

On Sunday evening, December 15, Taoiseach [Prime Minister] Enda Kenny delivered a public address thanking the Irish people for their sacrifices during 3 years of austerity.[2] The Minister for Finance Michael Noonan recently described the people of Ireland as the “real heroes and heroines” of the story. Yet, ominously, Mr Kenny also warned that a long road to recovery still lay ahead. [3]

The €25 billion ‘backstop’?

However, Mr Noonan also noted that all would be ok after the exit from the bailout, that there was no need to worry as the government was overflowing in cash to meet future obligations:

“Mr Noonan told the Fine Gael national conference the National Treasury Management Agency (NTMA) has built a €25bn fund which can act as a significant buffer after Ireland exits the bailout.”If we never borrowed another bob, we’re cash-funded into 2015,” Mr Noonan said. “Ireland is fortunate that the NTMA has almost €25 billion in cash balances as we return to the market so we have a backstop already in place.”” [4]

Yet, according to one commentator the sheer size of this €25 billion ‘backstop’ is itself yet another large cost to the Irish people:

“The National Treasury Management Agency (NTMA) is presently sitting on a cash mountain of nearly €25bn. It places it on deposit in the Central Bank of Ireland and receives interest at a rate of just 0.1% per annum – yes, just zero point one per cent! The €25bn is either borrowed or could be used to pay down borrowings which cost us an average of 3.5% per annum. In other words, this State is sitting on a cash mountain costing us €875m a year in interest and if you deduct the €25m we get from the Central Bank, in net terms this mountain of cash is costing is €850m! Per Year! And at the end of 2013, the funding from the €67.5bn external bailout from the so-called Troika comes to an end. And we have colossal borrowings which we need to repay – previously issued bonds and repayments to the Troika.” [5]

The EU-IMF bailout loans

And what about these ‘colossal borrowings’, the EU-IMF bailout loans? According to the European Commission – MEMO/13/457 regarding countries emerging from an EU-IMF bailout:

“Until they have paid back a minimum of 75% of the assistance received, they will remain subject to new enhanced surveillance. This is to ensure a successful and durable return to the markets as well as fiscal sustainability, to the benefit of the individual Member State concerned as well as the euro area as a whole.” [6]

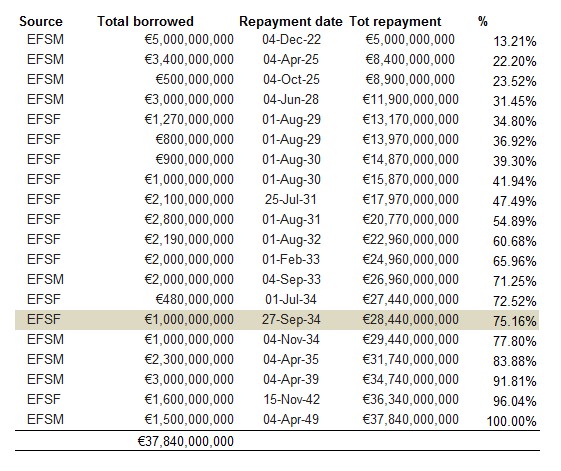

The extent and length of the indebtedness of the Irish state for the unforeseeable future as a result of the bailout has been examined by political correspondent Gavan Reilly who notes that:

“[On] the NTMA [National Treasury Management Agency] website you’ll see a list of the loans we’ve got from the two European bailout funds so far. Noting the repayment date for each (and adding seven years to each of the EFSM [European Financial Stabilisation Mechanism] repayment dates, because they haven’t yet finalised the extension to the repayment period), this is the schedule we get for the EU side of things: [see table below]

The line I’ve shaded in is the important one. If Ireland stopped borrowing from the EU this instant, and went back to the market of its own volition, it would take until September 2034 to repay the requisite 75%.” [7]

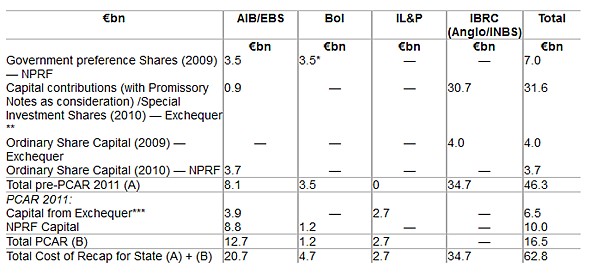

It is estimated that at least €62.8 billion has been poured into Irish banks so far and one single institution, the infamous Anglo Irish Bank, accounts for over €34.7 billion of socialised debt. [See table below]

http://karlwhelan.com/blog/?p=471

[IL&P = Irish Life and Permanent, Irish Bank Resolution Corporation = IBRC]

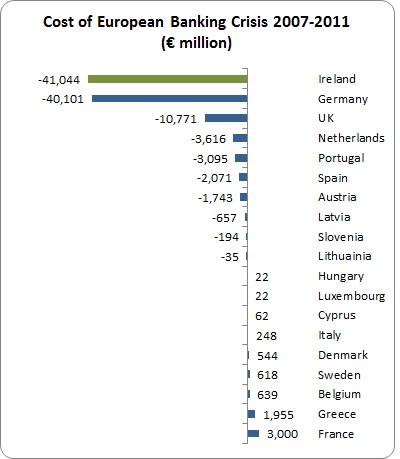

Cost of the European Banking Crisis

According to Michael Taft, Eurostat (the EU Commission’s data agency) has calculated the cost of the banking crisis in each EU country. He writes: “The Irish people have paid 42 percent of the total cost of the European banking crisis. The European banking crisis to date has cost every individual in Ireland nearly €9,000 each. The average throughout the EU is €192 per capita.” [8] [See table below]

http://www.thejournal.ie/readme/banking-crisis-bill-ireland-755464-Jan2013/

As I have written elsewhere, in 2007 Ireland’s general government debt was €47.2bn. It is estimated to be more than quadrupled to €205.9bn by the end of 2013. [9]

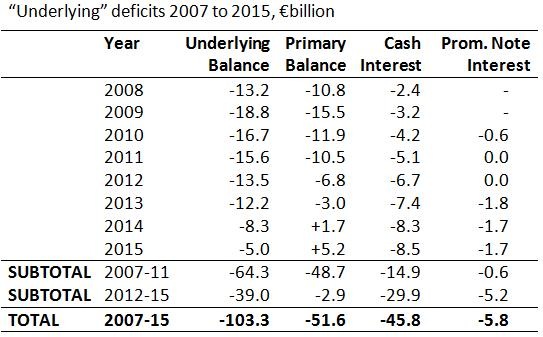

What is noticeable in government projected deficits is the increasing interest repayments for 2014 and 2015 while at the same time the projected surplus for the same years that will be achieved by more cutbacks showing that interest repayments on the huge debt are already beginning to grow to significant proportions. [See table below]

http://economic-incentives.blogspot.ie/2012/03/changing-nature-of-our-budget-deficits.html

[“underlying deficits” = deficits excluding direct payments to banks]

[Underlying Balance = Primary Balance + Cash Interest + Promissory Note Interest]

Ireland’s ‘pro-business environment’

So why has Forbes named Ireland as ‘best country for business’ this year? According to Forbes magazine:

“Despite these economic troubles, Ireland still maintains an extremely pro-business environment that has attracted investments by some of the world’s biggest companies over the past decade,” says the magazine.” [10]

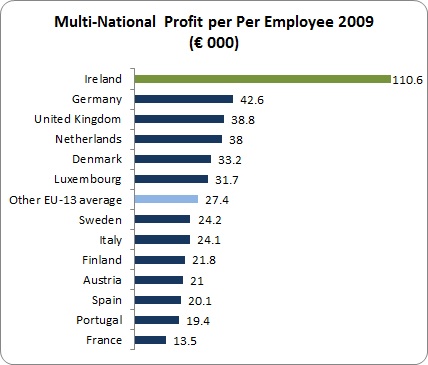

Despite [or because of] crippling debt burdens and cutbacks, productivity is one of the highest in Europe. According to Michael Taft: “Ireland is not just a league-leader, it is off the chart. MNCs here make more than four times the profit per employee than the average of the other EU-15 countries reporting (no data for Belgium or Greece). No wonder more and more multi-nationals are making Ireland their home.” [11] [See table below]

http://www.thejournal.ie/readme/corporation-tax-budget-674461-Nov2012/

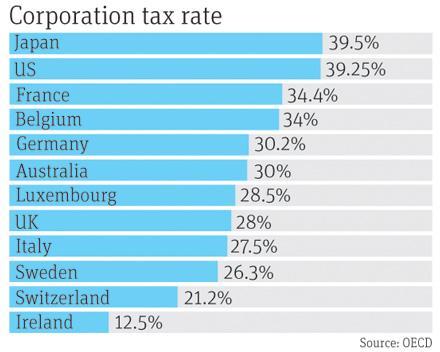

Low corporation tax rates: [See table below]

http://www.broadsheet.ie/2012/01/19/so-it-begins-7/

There is also the “Double Irish and Dutch Sandwich” tax-avoidance scheme (in which American-owned companies use Irish and Dutch subsidiaries to funnel profits into low- or no-tax jurisdictions)” [12]

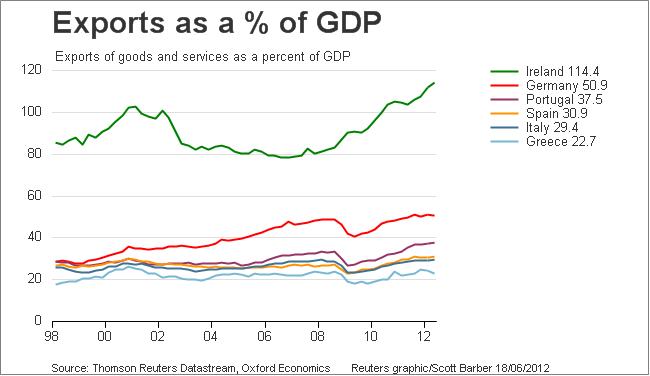

All these incentives result in Ireland being “the champion of exports in the Euro Zone. Germany takes a good second place and Portugal’s economy is also quite dependent on the international trade.” [13] Also the majority of Ireland’s exports are to EU member states and the advantages that that implies. [See tables below]

Exports as a Percentage of GDP 1998 – 2012

http://www.economicsinpictures.com/search/label/Ireland

Ireland’s Exports Partners 2009

http://www.economywatch.com/world_economy/ireland/export-import.html

Stable political and economic environment?

So how do Irish people benefit from all this attention and praise? There is relative political stability in Ireland (compared to the mass demonstrations against austerity in Spain and Greece) but this has come at a high price with the return of mass emigration and high levels of unemployment not seen since the 1980s. Yet despite the economic indicators of a modern thriving economy with high productivity and high exports, the Irish people are undergoing one of the most difficult economic contractions in Europe.

The exit from the bailout and the return to the capital markets means that Ireland is returning to the mutually beneficial relationship between the state and the private sector. The income sources for the state are various forms of public tax revenues and private sector bonds (55% of Government bonds are owned by non-residents as of June 2013). The advantaged private sector gets the interest on its bonds, low tax rates, government grants and political influence through lobbying.

However, the repayment of the massive EU-IMF bailout loans and interest may be setting the stage for an unsustainable exponential increase in cumulative debt especially if there is an increase in interest rates or another banking crisis. At home, high indebtedness, high mortgage debt and high mortgage arrears by households are putting the bailed-out banks under pressure. Meanwhile, abroad, the fragility of the eurozone and the global economy exerts its own pressures on economic confidence, an absolutely essential element in the world financial system. As the banking system slowly swallows the Irish economy like a python eating a deer, the Irish people still have the potential to end their own sacrifice on the altar of ‘austerity’.

Notes

[1] http://www.globalresearch.ca/austerity-is-a-scam-crisis-legislation-and-dodgy-debt-repayment-schemes/5322437

[2] http://www.rte.ie/news/2013/1215/492957-bailout-exit/

[3] http://www.irishtimes.com/news/politics/kenny-addressing-nation-as-state-exits-bailout-1.1628690

[4] http://www.independent.ie/irish-news/politics/noonan-to-meet-troika-after-budget-to-discuss-bailout-exit-29654885.html

[5] http://namawinelake.wordpress.com/2013/01/24/the-ntma-strategy-of-hoarding-cash/

[6] http://europa.eu/rapid/press-release_MEMO-13-457_en.htm]

[7] http://www.todayfm.com/mobile/index.php?id=2951

[8] http://www.thejournal.ie/readme/banking-crisis-bill-ireland-755464-Jan2013/

[9] http://www.globalresearch.ca/a-perfect-storm-brewing-for-irelands-economy/5358329

[10] http://www.irishtimes.com/business/forbes-names-ireland-as-best-country-for-business-1.1617277

[11] http://www.thejournal.ie/readme/corporation-tax-budget-674461-Nov2012/

[12] http://www.irishcentral.com/news/Leading-US-senators-push-Irish-government-to-fully-tax-Apple-Google-etc-231417211.html

[13] http://www.economicsinpictures.com/search/label/Ireland

For more information, graphs and tables on the Irish economy see:

Caoimhghin Ó Croidheáin (@cocroidheain) is a prominent Irish artist who has exhibited widely around Ireland. His work consists of paintings based on cityscapes of Dublin, Irish history and geopolitical themes (http://gaelart.net/). His blog of critical writing based on cinema, art and politics along with research on a database of Realist and Social Realist art from around the world can be viewed country by country at http://gaelart.blogspot.ie/.

|