The Obama administration may start its program to spur purchases of mortgage-backed securities from banks with about $20 billion in public and private money, down from as much as $100 billion when the effort was announced in March, sources said. The Treasury Department will pro vide about $1.1 billion in capital to eight to 10 money managers it will select for its Public-Private Investment Program.

[It is interesting that no mention is made of the fact that the Fed is creating (monetization) $3 trillion to purchase US Treasuries, Fannie Mae and Freddie Mac bonds and CDO toxic waste from banks. The Fed will not tell us what they are paying for the CDOs and part of the game is that the banks rotate the money into Treasuries, a sweet little daisy chain. As you can see, the Treasury might get an additional $20 billion into CDOs. We don’t see it happening. The private interests don’t want to get involved. Bob]

US consumers made 675,351 bankruptcy filings in the first half of 2009, a 36.5 percent increase from a year ago, according to the American Bankruptcy Institute. June filings by consumers totaled 116,365, up 40.6 percent from the same period in 2008, the ABI said.

Oracle plans to cut as many as 1,000 jobs in Europe, the CFDT labor union said on its Internet site. Of the total, about 250 jobs will be lost in France, equivalent to 16 percent of the company’s workforce there.

British authorities have started an investigation into millions of dollars of payments from the operations of the convicted money manager Bernard L. Madoff to companies linked to the Austrian banker Sonja Kohn, an Austrian official confirmed yesterday.

The Serious Fraud Office had asked Austrian prosecutors in May for help in investigating payments made by Madoff’s London office for research reports by Bank Medici, which was majority-owned by Kohn, who also served as its chairman.

“We’re closely cooperating with the SFO and the US Justice Department in that case,’’ the official, Gerhard Jarosch, a senior public prosecutor in Austria, said yesterday. A separate investigation by the Austrian prosecutor into whether Kohn and Bank Medici were involved with Madoff is continuing, he said.

Prosecutors are looking into whether Madoff paid more than $40 million to Kohn in exchange for turning three Bank Medici funds into feeder funds for his business, The Wall Street Journal reported, citing affidavits filed by prosecutors in the United States and Britain. The Austrian daily Der Standard reported last week that Kohn received about $11.5 million, for research reports for which prosecutors were unable to find receipts.

U.S. service industries from retailers to homebuilders contracted last month at the slowest pace in nine months, as measures of new orders and employment improved.

The Institute for Supply Management’s index of non- manufacturing businesses, which make up almost 90 percent of the economy, rose to 47 — higher than forecast — from 44 in May, according to data from the Tempe, Arizona-based group. Readings less than 50 signal contraction.

Our President favors torture just like his predecessor did. He threatens other governments if they expose what his administration is up too. He blocks any and all exposure of government activities, a culture of non-disclosure. In addition, there is a large list of dissidents, such as myself and other publishers and radio personalities of every political persuasion. Anyone who exposes what the Illuminists are up too is an enemy of the state. We wish George Orwell were here to see this.

Last week we filled you in on the scandal that could envelope and crush the administration. That is the illegal arbitrary dismissal of Investigator General Gerald Walpin who tried to get criminal charges brought against Barry’s close friend and Mayor of Sacramento, Kevin Johnson who misappropriated some $500,000. The AG later layed a $73,000 payback on Johnson. As you can see, crime pays. More blatant corruption. We have done scores of programs on the mainline media regarding the scandal, something the kept media themselves refuses to do.

Sir Alan Greenspan was a disaster for America. His latest lying, idiotic comment was, “I don’t think it is an economic problem – it is a political problem.”

What we have is a monetary and fiscal problem that translates into an economic problem. The American engine of growth has grounded to a halt over the past two years as a result and has taken the entire world economy with it. Today’s problems are very much an out growth of Greenspan’s terribly flawed monetary management, followed by an equally incompetent Ben Bernanke.

What else would you call non-financial growth in the early nineties, which averaged $565 billion annually that peaked at $3.545 trillion in 2007? Does that sound like monetary sanity? This was the massive system of credit that inflated asset prices, incomes, corporate profits and government revenues. This caused the wild orgy of consumption, services, including de-industrialization and massive imports spawned by free trade, globalization, offshorting and outsourcing. Those horrendous events will take decades to reverse. Who can call prudent or reasonable the creation of those combined Treasury, GSE and MBS obligations surging $1.949 trillion, or 15.3% in 2008 to $14.709 trillion? This is called Ponzi finance dynamics. The word is bubble and that bubble is still being sustained. How does Sir Alan justify Total Mortgage Debt growth from the 90s averaging $269 billion to $1 trillion by 2003 and $1.390 trillion in 2006? ABC, asset backed securities, went from $200 billion in 2003 and beyond $800 billion in 2006. MBS doubled in four years to $4.5 trillion by the end of 2007.

That was the bad news; unfortunately there is worse news on the way. Today’s credit crisis finance bubble will make the residential and commercial bubble look like a joke. Multiply by 5 or 10. Who knows where this can end up? The bomb is in the air and hasn’t even hit yet. The quality of Treasury, GSE (Fannie Mae and Freddie Mac), CDO and ABS falls every day. The debt is massive and it is not producing real economic wealth creation. This is a tremendous drag on the system. Wage increases are miniscule, inflation grows as purchasing power falls as does general confidence. There is major misallocation of assets and a maladjusted economic structure that can only end in dire inflationary consequences.

The private creation of real jobs has generated about 100,000 jobs a year and the public sector more than double that, or 240,000 a year. Most jobs created over the past ten years have been low paying. 290,000 have been created in healthcare, 157,000 in food and drinking establishments and 139,000 in government education. Declining jobs, free trade, globalization, offshoring and outsourcing, have decimated living standards and have caused a massive transfer of wealth to BRICs; OPEC and slave labor countries that cheapen their currencies by manipulating them and by subsidizing their industries. In just the first quarter GDP fell 5.5% due to a decline in inventories and trade. The 37.3% decline in business investment and inventories was a record. The greatest decline since 1947 when records began. The 38.8% decline in homebuilding is the largest contraction since 1980.

Next comes the planned reduction of Fed market support programs, including swap lines with 14 international central banks, due to expire in October to February. The Fed says it will reduce the maximum size of its term securities lending facilities, TSLF, from $200 billion plus options, and the maximum size of its term auction facility, TAF, to $500 billion from $600 billion. This is part of the Fed’s glide path to normalization. This rhetoric can’t happen unless the Fed has finally decided to allow deflation to take over and we do not see that happening.

On of the more instigators of our current credit crisis, Goldman Sachs, are now recording record bonuses in the greatest financial crisis in almost 80 years.

This success by Goldman is not shared throughout the industry. The walls of capitalism are falling and Goldman is making a fortune. We ask how? The answer is inside information and that they are even more corrupt than Washington is. Goldman is part of a triumphinit that rules America although few Americans are aware of their power – a power that sucks the very lifeblood out of our country and has for at least the last 100 years. These people and others have controlled our country for a long time. It is a marriage made in hell. Many country’s politicians and Wall Street and bankers control money and in turn control almost every nation today.

This past April we saw tax reductions and increased benefits of $121 billion on an annualized basis. As a result consumer spending increased by a paltry $1 billion. In May, stimulus was $163 billion and consumer spending only increased by $25 billion. As a result personal savings jumped from 4.3% in March, 5.6% in April and 6.9% in May.

This result needless to say is not what the Frankenstein elitists in Washington had in mind. The next step, of course, is to force consumers to spend, otherwise the consumer cycle won’t work. The public is spending $0.08 of every stimulus dollar and the rest is being used to pay down debt or is going into savings. We predicted 90% would not be spent and again we were right, that means as a percentage of GDP only 70% is coming from the consumer, down from 72% at the peak.

The stimulus package did another thing and that is distort income in the second quarter resulting in income gains of 1.4% in May. The year-on-year trend is still -1.1%.

This year 5% of workers took unpaid leave and 15% had to accept a pay cut. Ten percent had to take an extra job last year and 20% of 45 to 54-year olds took second jobs.

Between now and 2013, $5 trillion in wealth will have to be liquidated. A good part of that will occur over the next 3-1/2 years. That means continued monetization and depression and an ever-depreciating dollar. This depression will last 8 to 20 years.

The workweek has fallen to 33.1 hours. We see that number below 30 next year.

Probably more than 50% of workers will stop funding 401(k)’s, IRA’s and Roth’s. Twenty-five percent of companies are suspending 401(k)’s and that number will grow. That will have a devastating affect on the stock and bond markets. Again, get out of all stocks except gold and silver shares and Canadian Treasuries. Get out of corporate bonds. Interest rates will rise over the next two years. Get rid of cash value life insurance policies and annuities. No CDs of any kind. Unemployment has doubled in seven months from 7 to 14 million. In the previous eight years, due to free trade, globalization, offshoring and outsourcing, we lost 5 million jobs. We are calling U6 unemployment at 20.5%. Officially it is 16.5%. Even the Center for Labor Market Studies at Northeastern University says real unemployment is 18.2%.

Our President is just realizing that he is presiding over the bankruptcy of the US. In order to bring this to a halt he would have to cut mandatory programs that underline the welfare state, which makes up 60% of the budget. We see no chance of that happening. That means in the next three years the Treasury will go broke. Once the insolvency occurs welfare, Social Security and Medicare will end along with many other programs. Imperial America will cease to exist. Those occupations in Japan, South Korea, Europe, Iraq, Afghanistan and hundreds of other bases, will end, unable to be financed. The burden will be too much to any longer bare.

How can any national government expect to survive fiscally as tax revenue falls 18% and spending increases 18%? All the players know this, so the only conclusion we can come to is that they want our government to collapse. Worse yet, spending won’t be the official $1.84 trillion, but $2 to $2.5 trillion. Corporate tax revenues have fallen 61% and individual returns are off 22% as of May. The US government and the Fed are committed to spend $12.8 trillion, but if we add in further Fed monetization declared to be created by 9/30/09, that figure will be closer to $15.8 trillion. This is much greater than our entire GDP for last year. As a result the 30-year bond is off almost 30% this year, and the 10-year note has lost 11%. Overall all Treasuries are off more than 6% and that is while the Fed has been manipulating the bond market. While all this has transpired the dollar has fallen from 89.5 on the USDX to 79.9 – that is close to 10%. Thus, if you owned 10-year T-notes you have lost 20% of your capital, plus the inflation loss of 9%. You are a net loser of some 30%. Two types of investors buy T-bills, or bank CD’s, they are either dumb or they have a vested interest in not seeing the system collapse.

Buyers of treasuries and Agencies cannot absorb these losses indefinitely. This has been going on for 9 years. From this level we believe losses could be the intrinsic value of all the funds invested. One is certainly looking at in excess of a 60% loss in purchasing power. The average foreign nation holds 64.5% of their reserves in US dollars. That should break just about everyone.

As a result of this profligate mayhem other nations have begun barter exchanges. That is Russia with Europe, China and Brazil. If Cap and Trade is passed by the Senate the cost of imports will rise 20% and foreigners will refuse to accept US dollars in payment. If the US does not comply with foreign currencies or barter they will not be able to purchase oil. The US imports 65% of its oil needs, perhaps more. We won’t have much to barter with, because we do not have the export numbers we once had.

Unemployment will rise into 2013. What will we do with 150,000 people entering the labor force annually? Fifty-three percent of workers let go were fired permanently. Four million jobs in construction, financial services, durable goods manufacturing and leisure and hospitality won’t come back for a long time. Official overall male unemployment supposedly is 10.5%, for those 20 to 24, 15% and for those 16 to 19 it is 23%.

The Dow is going to 2,800 to 3,200, if we are lucky. We are not in a new bull phase, as CNBC and others would have us believe. All indicators point to a market breakdown. You can take that to the bank.

Deflation has been an underlying factor in the world economy for six years. It has been temporarily overcome by zero interest rates and the creation of massive amounts of money and credit worldwide.

The CRB fell 53% and is now off 39% and international shipments are yet to recover.

As a dollar solution China, Russia and Brazil are pursuing SDR’s, IMF Special Drawing Rights, which are not worth the paper they are written on. Now the IMF wants to issue fiat bonds based on fiat currencies. If issued the bonds will not trade in the open market, only between central banks. Who we ask will absorb all the toxic waste? The answer is the make believe bank known as the IMF. The switch would be another prolongation of the crisis. Our guess is the US Treasuries will be delivered to the Treasury, the IMF will be credited, and the Treasuries won’t reenter the trading system and just be deposited by passing monetization. That is pretty slick, but it won’t solve any problems in the long run. This does not mean Treasury auctions will cease. We expect the exchange of US Treasuries will be from present holders who want to be out of dollar denominated securities, such as China. It is no more than a game of musical chairs.

As you know the Treasury currently is in the process of buying and monetizing $300 billion in treasury debt. We wrote two months ago that figure would increase to $1 trillion by 9/30/09. The administration and congress have no intention of cutting spending. When the system collapses it will be far worse than it should have been.

This is the way Barry Saetoro does business along with his Bilderberger-CFR pals. You wanted change, you got it. It is debt that will bankrupt our nation and turn our country into chaos. As his predecessor did, our president has followed in his footsteps by using secrecy to cloak fiscal chicanery and outright illegal actions. Corruption and cronyism are already flourishing on his watch. Just look at the scandal in the firing and resignations of Investigators General. You hear little or nothing in the mainline media regarding the corruption. You hear nothing about the 244 co-sponsors of Ron Paul’s HR 1207, ”the Federal Reserve Transparency Act of 2009.” All we hear are lies, disinformation, propaganda and omission of anything important. Washington and Wall Street do the same. Americans are being spied upon by their own government on an ever-increasing basis. To think we once worked in conjunction with the National Security Agency some 51 years ago when it was in its infancy. It has turned into a monster.

Cash strapped states are delaying sending out millions of dollars in tax refunds due to plummeting tax revenue. In addition states in order to save money have cut personnel and some have been cut in the tax department.

California which has a deficit of more than $24.3 billion is issuing $3 billion in promissory notes that are not worth the paper they are written on.

Government, Wall Street and corporate America tell us an economic recovery is on the way. If that is so, why are corporate insiders dumping the shares of the companies they run? It is because they believe corporate earnings are going to be dreadful. Those earnings reports start being released in two weeks.

The economy should be slightly strong this year and slightly stronger than that in 2010. The big problem will be a falling dollar and the threat of debt default. If you listen to Wall Street, government, corporate America and our media, you will be left in the dust.

Even another $2 trillion stimulus package won’t work. All it will do is keep growth neutral for a year buying more time, as monetary inflation rages.

September and October is when the crisis should hit. This will not be a major crisis, but a crisis never the less. This will be but a trial run. After two years nothing has been fixed. All that was accomplished was a taxpayer bailout of banks, Wall Street, insurance companies and GM and Chrysler.

The average recession since 1900 lasted just over 14 months. We were in recession for two years as of February and in depression for four months.

Along with a fall in the dollar we could very well see debt defaults. In addition, we have unemployment at 20.5% and we will see lots more bankruptcies.

Referring back to the Bilderberg meeting in Greece several weeks ago their most important concern was loss of control and that they should attempt to close out the depression as soon as possible, and abandon any reforms or attempts to institute a world government and currency. There is no question their monetary system is disintegrating, business domestically and internationally continues to look dreadful, and companies continue to layoff employees worldwide. All over the world banks and companies will be failing with the US and UK leading the pack. This, again, is why you do not own CDs, and only keep operating expenses for 3 to 6 months at a bank. Have $5,000 in small bills at home and all other assets in gold and silver coins and shares. The stock and bond markets will eventually collapse, so be out of bond, stocks, except for gold and silver shares, and out of cash value insurance policies and annuities.

Politicians, professional investors, public investors and the public are going to be shocked at what is going to happen and they are ill-prepared to defend themselves and their wealth. The entire world will be on stimulus packages. As banks and Wall Street become more insolvent political leaders will see stage 2 of the depression appear as the Fed and Treasury flood the world with money.

We mentioned several weeks ago that Supreme Court nominee Sonya Sotomayor belonged to the Belizean Grove, the female equivalent of the male Bohemian Grove. They hold their meetings in Belize. The Judge has since resigned. We wonder if the ladies version practices what the men practice. Occult worship, orgies and Satin worship?

There are just two factors holding up world stock markets, manipulation and massive amounts of money being poured into the system by governments and central banks. Everyone is standing by waiting to see what success the many stimulus packages will bring, as stock markets worldwide go into a stall after having risen 40 to 50 percent.

A few weeks ago EU central banks injected $5.2 trillion into their banking system, while the US committed for $14.8 trillion. The US Treasury will have to raise over $3 trillion in debt this year of which $1 trillion will be monetized.

Fed credit has expanded $1.178 trillion yoy, or 134%. It now totals $2.055 trillion. Treasury debt obligations are $2.177 trillion, up 16.6% yoy, and you haven’t seen anything yet. Your great, great, great grandchildren will pay back this debt, so we can bail out insolvent banks, Wall Street, insurance companies and manufacturing companies. People who do these sort of things are unhinged.

The Fed has been saving financial institutions for two years now. They have been totally unsuccessful. In just the first quarter household wealth fell $1.3 trillion that is versus a $4.9 trillion loss in the last quarter of 2008, or a $6.2 trillion loss in six months.

Bank lending to borrowers is $9.722 trillion, up $317 billion yoy. For the first six months of 2008, bank credit has fallen almost $200 billion. The economy cannot gain momentum unless banks increase lending, because 92% of the direct stimulus has been used to pay down debt.

American industrial capacity shows 35% of equipment idle and world trade has fallen 50% over the last two years. Foreigners, such as China and India, already have decimated our economy with slave-produced goods. Tariffs have to be put in place or we will have no jobs left.

Trade war is already underway and we cannot compete unless we drop wages from $16.00 an hour to $3.00 an hour. Now you can see how transnational conglomerates, such as Wal Mart, IBM and others are ripping us off. Look at the profits, which are shipped to the Cayman Islands where they pay 2% in taxes. The last time, four years ago, that they brought $350 billion back, they didn’t pay 35% taxes, they paid 5-1/4%. Thanks to our purchased Congress and a promise to create jobs. They never created any – another handout to the elitists. Mark our words global trade will come to a halt over the next three years and it is about time.

It is only a matter of time until calamity hits world markets. The first target is a fall in the value of the dollar, then the failure of a major bank somewhere around the world. Probably in the US, UK or Europe just like Creditanstalt in the late 1920s. Like in the US and Europe in the 1930s loans are going to be recalled, and that is already underway. The FDIC cannot help – they have $13 billion although they have asked Congress for $500 billion more. We have told you over and over again, no bank CDs and only keep 3 to 6 month’s funds for operation in a bank or credit union. Have at least $5,000 in small bills in your safe at home along with your gold and silver coins and weapons. Do not forget a water filter and freeze dried and dehydrated food for six months. The stock market is going to tank further and zero interest rates won’t last forever. As rates rise, bonds fall.

The freefall on the market should begin again before the end of October and a revisit to 6,600 is what we see. When it visited there on March 9th, it had fallen 53.5% from its all time high. A break to that level or lower levels would put every bank, brokerage house, insurance company and pension plan in acute jeopardy. The current bear market rally is somewhat like the market rally in 1931. This rally has been topping out for two months and it is only a matter of when it will fall. We are seeing massive insider selling just as we did when the Dow hit 14,164. These corporate CEO’s tell us everything will be just fine as they flee the market. The bank and brokerage indexes are starting to head down again, off some 20%. They were among the leaders on the way up.

Essentially what the Fed has done with zero interest rates is create another bubble and that will end badly, not only in the US but in many other countries as well. This means hyperinflation is on the way and as we have said before there will be no attempt to reverse course and impose tightened liquidity conditions. This bubble will be much bigger and even more devastating then the mortgage finance bubble. The mortgage bubble lasted five years, but because of government dependency on the Fed and foreign lenders this could happen more quickly – say in two to three years.

The Fed is controlling the financial system and they caused this disaster. The only solution is passage of HR 1207 and S 604 – The Federal Reserve Transparency Act of 2009. Then pass legislation to end the Fed. Then we can get this mess sorted out once and for all.

The morons in Sweden have cut interest rates to a minus .25%. Pretty soon they will throw money out of helicopters.

This is another step toward trade wars.

Mortgage lenders don’t try to rework most home loans held by borrowers facing foreclosure because it would probably mean losing money, a study released yesterday by the Federal Reserve Bank of Boston concludes.

The Boston Fed’s findings suggest the Obama administration’s major effort to solve the foreclosure crisis by giving the lending industry $75 billion to rewrite delinquent loans to more affordable levels is not likely to work.

One of the study’s coauthors, Boston Fed senior economist Paul S. Willen, said the government would be better off giving the money directly to struggling borrowers to help them with their payments, rather than to lenders that are averse to working out the troubled loans.

The U.S. Federal Reserve, facing growing pressure as it tries to heal the ailing economy, dodged a bullet on Monday when the U.S. Senate cast aside a new effort to increase scrutiny of the central bank.

On procedural grounds, the Senate blocked a bid to permit the U.S. comptroller general, who heads the investigative arm of Congress known as the Government Accountability Office, to audit the Federal Reserve system and issue a report.

Republican Senator Jim DeMint, who has been pushing for greater transparency at the Fed, failed to get the provision attached to the must-pass annual spending bill that includes funding for the GAO for the upcoming 2010 fiscal year.

The audit would have included details about the Fed’s discount window operations, funding facilities, open market operations and agreements with foreign central banks and governments, DeMint said on the Senate floor.

“The Federal Reserve will create and disburse trillions of dollars in response to our current financial crisis,” DeMint said. “Americans across the nation, regardless of their opinion on the bailout, want to know where the money has gone.

“Allowing the Fed to operate our nation’s monetary system in almost complete secrecy leads to abuse, inflation and a lower quality of life,” he said.

Democrats who control the Senate blocked the South Carolina Republican’s amendment on the grounds that it violated rules prohibiting legislation attached to spending bills.

Fed officials were not immediately available to comment.

The move comes as some lawmakers have increasingly become wary of the Fed’s actions, particularly for its handling of the real estate market and the meltdown of major financial institutions like investment bank Bear Stearns and insurance giant American International Group.

A non-binding provision in the fiscal 2010 budget blueprint Congress approved in April called on the Fed to provide more information about collateral posted against Bear Stearns and AIG loans.

That measure also sought a study evaluating the appropriate number and costs of the regional Fed banks.

The U.S. central bank has a seven-member board in Washington whose members are nominated by the president and confirmed by the Senate. It also has 12 regional banks whose presidents are appointed by banks and other businesses in their local districts, with the consent of the Washington board.

The vacancy rate rose to 10.2 percent in the second quarter from 8.5 percent in the first quarter in the District, to 13.9 percent from 12.9 percent in Northern Virginia; and to 13.9 percent from 13.1 percent in suburban Maryland.

In June, AT&T was singled out for avoiding state income taxes on millions of dollars of earnings by sending the money out of Connecticut to a subsidiary in another state.

But it’s not the only business doing that.

As state legislators grapple with a two-year budget deficit estimated at just under $9 billion, multi-state corporations are using loopholes in Connecticut’s tax law to legally divert tens of millions of untaxed dollars out of Connecticut as “intercompany royalties,” tax experts say.

It’s a practice in which a company essentially pays itself untaxed money for use of its own logo on buildings, stationery and so forth. Because corporate tax information is confidential, it’s unclear how many other companies are avoiding taxes that way.

“These companies pay less in taxes than the people who sweep their floors at night and type their letters,” said Richard Pomp, a University of Connecticut law professor and expert on business taxes. “It’s a scandal. My guess is every one of the big corporations is doing it in Connecticut.”

AT&T’s use of the practice came to light because the state Department of Public Utility Control audits the financial statements of a company subsidiary, AT&T Connecticut. According to DPUC documents, between June 2002 and December 2004, AT&T Connecticut sent $145 million in royalties to a company AT&T owns in Nevada, where the money was not subject to corporate taxes.

Connecticut Attorney General Richard Blumenthal announced in June that he has begun investigating AT&T’s use of the practice.

Tax-reform advocates say the tactic shortchanges Connecticut out of millions of dollars in tax revenue every year. Corporations call it smart business.

“There’s nothing wrong with good tax planning,” said corporate tax attorney Morris W. Banks, of Pullman & Comley in Hartford, of the practice.

The issue has drawn extra attention recently as revenue-starved states and corporations joust during the recession.

Who wins the battle between Connecticut and AT&T is still to be determined. But the U.S. Supreme Court’s recent refusal to hear a similar case from Massachusetts could indicate Connecticut may have the upper hand.

Money goes elsewhere

Blumenthal charged in June that while AT&T was “pleading poverty” and cutting jobs in Connecticut, it was busily avoiding state taxes by sending money to Nevada.

All corporations that “carry on business” in Connecticut are subject to the state’s 7.5 percent corporate tax, although what constitutes “doing business” is routinely debated in court. Some corporations have claimed that they should not have to pay state taxes unless they have a “physical presence in the state.”

According to AT&T financial statements, a corporate subsidiary, AT&T Connecticut, has for years been paying Reno, Nev.-based Knowledge Ventures, also owned by AT&T, for the use of AT&T trademarks, such as the company’s blue-and-white globe logo that’s printed on customer bills. In 2008, the company paid Knowledge Ventures $46.7 million in “intercompany royalties.”

AT&T has said the payments are a common and acceptable practice, and they do not come from rates paid by customers.

“Substantially all of AT&T’s domestic subsidiaries that earn revenue from external customers pay royalties to our intellectual property subsidiary,” wrote company spokesman Chuck Coursey in an e-mail. “The royalty payments cover the use of all of AT&T’s intellectual property (for example, trademarks, trade names, patents).”

Coursey said the Nevada holding company manages all of the company’s royalties, including those paid by third-party companies unrelated to AT&T.

Blumenthal, however, has criticized AT&T for the practice, saying it “questionably siphoned” the money away from Connecticut’s taxpayers and consumers. His office learned about the royalties from a routine audit of the company’s financial statements conducted for the state DPUC. The chairman of the DPUC wrote a letter to the state tax commissioner in May, alerting her to the untaxed payments.

“These matters are obviously outside of the department’s jurisdiction or expertise,” wrote DPUC Chairman Donald W. Downes in the letter.

“However, the department believes that your agency should be apprised of the royalty payment arrangement so that you might investigate to ensure that equity prevails among Connecticut taxpayers.”

Mr. Williams on the goofy B/D Model: The system was not designed to accommodate recessions, but the benchmark revisions tended to show a pattern of fairly consistent overstatement with the annual revisions, regardless of the business cycle. During the reporting cycle covering the 1990 to 1991 recession, a particularly large downward benchmark revision in previously reported payrolls levels was blamed partially on the BLS assuming that companies that had stopped reporting during the recession still were in business, with proportionate payroll employment attributed to them by the BLS. The problem was that much of the non-reporting reflected companies going out of business. The bulk of that modeling was based on periods of economic growth. [John believes that the Birth/Death Model has overstated employment by 2.5 million jobs per year.]

The unadjusted annual decline in June payrolls was the deepest since a similar decline at the trough of the 1958 recession, but still shy of the 4.9% trough seen in the 1949 downturn. When the 1949 annual low growth is broken, possibly next month, the annual percentage contraction in payrolls will be the most severe since the production shutdown following World War II.

The unemployment timebomb is quietly ticking Beyond riots in Athens

and a Baltic bust-up, we have not seen evidence of bitter political protest as the slump eats away at the

legitimacy of governing elites in North America, Europe, and Japan. It may just be a matter of time…

The Centre for Labour Market Studies (CLMS) in Boston says US unemployment is now 18.2pc, counting the old-fashioned way. The reason why this does not “feel” like the 1930s is that we tend to compress the chronology of the Depression. It takes time for people to deplete their savings and sink into destitution.

Did someone try to steal Goldman Sachs’ secret sauce?

While most in the US were celebrating the 4th of July, a Russian immigrant living in New Jersey was being held on federal charges of stealing top-secret computer trading codes from a major New York-based financial institution—that sources say is none other than Goldman Sachs…

The platform is one of the things that apparently gives Goldman a leg-up over the competition when it comes to rapid-fire trading of stocks and commodities. Federal authorities say the platform quickly processes rapid developments in the markets and uses top secret mathematical formulas to allow the firm to make highly-profitable automated trades.

The criminal case has the potential to shed a light on the inner workings of an important profit center for Goldman and other Wall Street firms…

The case against Aleynikov may explain why the New York Stock Exchange moved quickly last week to stop reporting program stock trading for its most active firms.

A Themis Trading LLC White Paper

We believe, however, that there are more fundamental reasons behind the explosion in trading volume and the speed at which stock prices and indexes are changing. It has to do with the way electronic trading, the new for-profit exchanges and ECNs, the NYSE Hybrid and the SEC’s Regulation NMS have all come together in unexpected ways, starting, coincidently, in late summer of 2007.

This has resulted in the proliferation of a new generation of very profitable, high-speed, computerized trading firms and methods that are causing retail and institutional investors to chase artificial prices.

These high frequency traders make tiny amounts of money per share, on a huge volume of small trades, taking advantage of the fact that all listed stocks are now available for electronic trading, thanks to Reg NMS and the NYSE Hybrid. Now that it has become so profitable, according to Traders Magazine, more such firms are starting up, funded by hedge funds and private equity (only $10 million to $100 million is needed), and the exchanges and ECNs are courting their business.

This paper will explain how these traders – namely liquidity rebate traders, predatory algorithmic traders, automated market makers, and program traders – are exploiting the newmarket dynamics and negatively affecting real investors.

In this case, our institutional investor is willing to buy shares in a price range of $20.00 to $20.05. The algo gets hit, and buys 100 shares at $20.00. Next, it shows it wants to buy 500 shares. It gets hit on that, and buys 500 more shares. Based on that information, a rebate trading computer program can spot the institution as having an algo order. Then, the rebate trading computer goes ahead of the algo by a penny, placing a bid to buy 100 shares at $20.01. Whoever had been selling to the institutional investor at $20.00 is likely to sell to the rebate trading computer at $20.01. That happens, and the rebate trading computer is now long 100 shares at $20.01 and has collected a rebate of ¼ penny a share. Then, the computer immediately turns around and offers to sell its 100 shares at $20.01. Chances are that the institutional algo will take them.

The rebate trading computer makes no money on the shares, but collects another ¼ penny for making the second offer. Net, net, the rebate trading computer makes a ½ penny per share, and has caused the institutional investor to pay a penny higher per share.

Last week, the stock market tumbled on news that housing foreclosures and delinquencies rose again in the first quarter. The Office of the Comptroller of the Currency said that among the 34 million loans it tracks, foreclosures in progress rose 22 percent, to 844,389. That figure was 73 percent higher than in the same period last year.

Foreclosures, meanwhile, keep rising. In June, 281,560 were in process, slightly above the 277,847 in May. Last January, there were about 242,000 foreclosures in the pipeline among the Wells Fargo trusts. “I was hoping we would see some impact in June of the government’s program,” Mr. White said. “Is ‘Home Affordable’ working? My short answer is no.”

Though few people have heard of it, hot money — or brokered deposits, as it is also known in the industry — is one of the primary factors in the accelerating wave of failures among small and regional banks nationwide. The estimated cost to the Federal Deposit Insurance Corporation over the last 18 months is $7.7 billion, and growing.

The 79 banks that have failed in the United States over the last two years had an average load of brokered deposits four times the national norm .

An investigator at the Securities and Exchange Commission warned superiors as far back as 2004 about irregularities at Bernard L. Madoff’s financial management firm, but she was told to focus on an unrelated matter, according to agency documents and sources familiar with the investigation.

Walker-Lightfoot’s supervisors on the case were Mark Donohue, then a branch chief in her department, and his boss, Eric Swanson, an assistant director of the department, said two people familiar with the investigation. Swanson later married Madoff’s niece, and their relationship is now under review by the agency’s inspector general, who is examining the SEC’s handling of the Madoff case.

New Evidence on the Foreclosure Crisis; Zero money down, not subprime loans, led to the mortgage meltdown

51% of all foreclosed homes had prime loans, not subprime, and that the foreclosure rate for prime loans grew by 488% compared to a growth of 200% for subprime foreclosures.

The analysis indicates that, by far, the most important factor related to foreclosures is the extent to which the homeowner now has or ever had positive equity in a home.

Homeowners across the country are challenging their property tax bills in droves as the value of their homes drop, threatening local governments with another big drain on their budgets.

The tax appeals and reassessments present a new budget nightmare for governments. In a survey conducted by the National Association of Counties, 76 percent of large counties said that falling property tax revenue was significantly affecting their budgets, said Jacqueline Byers, the association’s research director.

Officials in some states say their property tax revenue is falling for the first time since World War II.

At a court appearance July 4 in Manhattan, Assistant U.S. Attorney Joseph Facciponti told a federal judge that Aleynikov’s alleged theft poses a risk to U.S. markets. Aleynikov transferred the code, which is worth millions of dollars, to a computer server in Germany, and others may have had access to it, Facciponti said, adding that New York-based Goldman Sachs may be harmed if the software is disseminated.

“The bank has raised the possibility that there is a danger that somebody who knew how to use this program could use it to manipulate markets in unfair ways,” Facciponti said, according to a recording of the hearing made public today. [The prosecutor apparently does not understand the implications of his statement but most of The Street and much of the public do.]

Mortgage applications in the U.S. rose last week as refinancing jumped by the most since March and purchases climbed to the highest level in three months.

The Mortgage Bankers Association’s index of applications to purchase a home or refinance a loan increased 11 percent to 493.1 in the week ended July 3, from 444.8 in the prior week. The group’s refinancing gauge surged 15 percent, while the index of purchases gained 6.7 percent.

Foreclosure-driven declines in prices have brought more homes within reach of buyers who qualify for credit, helping to stabilize demand. At the same time, unemployment is rising and borrowing costs are edging back up, indicating any rebound for the housing industry will be slow to take hold.

“Prices are coming off toward more affordable levels,” said David Semmens, an economist at Standard Chartered Bank in New York. While sales are “showing some stability,” he said, “we don’t expect the housing market to suddenly turn around.”

Today’s report showed the mortgage bankers’ refinancing gauge increased to 1,707.7 from the previous week’s 1,482.2, which was the lowest reading since November 2008. The purchase index rose to 285.6 from 267.7.

In a sign the housing slump may be bottoming out, a July 1 report from the National Association of Realtors showed the number of Americans signing contracts to buy previously owned homes rose in May for a fourth consecutive month.

The share of applicants seeking to refinance loans climbed to 48.4 percent of total applications last week, today’s report showed, from 46.4 percent.

National chain store sales fell 4.3% in the first five weeks of June versus the previous month, according to Redbook Research’s latest indicator of national retail sales released Tuesday.

The latest numbers are starkly different from recent weeks because they don’t include Wal-Mart Stores Inc. (WMT), which said last month it would no longer provide monthly sales figures.

The fall in the index was compared to a targeted 4.1% drop.

The Johnson Redbook Index also showed seasonally adjusted sales in the period were down 4.4% compared with June 2008, compared to a targeted 4.2% fall.

Redbook said that on an unadjusted basis, sales in the week ended Saturday were down 4.2% from the same week in 2008 after a 4.3% decline the prior week.

Soaring U.S. unemployment and a shrinking economy drove delinquencies on credit card debt and home equity loans to all-time highs in the first quarter as a record number of cash-strapped consumers fell behind on their bills.

Delinquencies on the value of all card debt soared to a record 6.60 percent from 5.52 percent in the fourth quarter as more cardholders relied on plastic to meet day-to-day expenses, the American Bankers Association said.

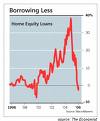

Late payments on home equity loans rose to 3.52 percent from 3.03 percent, and on home equity lines of credit climbed to 1.89 percent from 1.46 percent.

A broader gauge showing late payments on eight categories of loans rose for a fourth straight quarter to a new record, edging up to 3.23 percent from 3.22 percent. That rate actually understates consumer pain because it excludes credit cards. The ABA tracks loan payments that are at least 30 days late.

The International Council of Shopping Centers and Goldman Sachs Retail Chain Store Sales Index edged up 0.1% in the week ended Saturday from its level a week before on a seasonally adjusted, comparable-store basis.

On a year-on-year basis, retailers saw sales rise 0.5% in the latest week.

Despite massive government efforts to bolster the credit market, banks are pulling back severely on card lending.

In the first four months of the year — the latest data — banks issued 9.8 million new credit cards, a 38% drop from the same time last year, according to Equifax credit bureau data. Low-risk borrowers can still get credit, but they’re getting less than before. The average limit on a new card, after rising during the recession, slipped 3% so far this year to $4,594.

Home prices may fall in more than half of the largest U.S. cities through the first quarter of 2011 as unemployment and foreclosures rise, mortgage insurer PMI Group Inc. said.

Thirty of the 50 biggest metropolitan areas have at least a 75 percent chance of lower prices through March 31, 2011, Walnut Creek, California-based PMI said in a report today. The decline is likely to spread to “all regions of the nation” from California, Florida, Nevada and Arizona, the states most affected by the housing slump, PMI said. “The housing market has been hit by a demand shock of high unemployment and a supply shock of distressed foreclosure sales,” LaVaughn Henry, senior economist at PMI, the fourth- largest U.S. mortgage insurer, said in an interview.

The United States should be planning for a possible second round of fiscal stimulus to further prop up the economy after the $787 billion rescue package launched in February, an adviser to President Barack Obama said.

“We should be planning on a contingency basis for a second round of stimulus,” Laura D’Andrea Tyson, a member of the panel advising President Barack Obama on tackling the economic crisis. said on Tuesday.

Yesterday the Fed bought, which is a euphemism for monetized, $7B of Treasuries maturing between January 2014 and March 2016 even though the US Treasury will hold a one-week record of four auctions this week to issue $73B of US debt. $8B of 10-year inflation-linked notes was sold yesterday. The remaining tranches: $35B of 3s today, $19B of 10s on Wednesday and $11B of 3s on Thursday.

Investment banks, including Goldman Sachs and Barclays Capital, are inventing schemes to reduce the capital cost of risky assets on banks’ balance sheets, in the latest sign that financial market innovation is far from dead.

The schemes, which Goldman insiders refer to as “insurance” and BarCap calls “smart securitisation”, use different mechanisms to achieve the same goal: cutting capital costs by up to half in some cases, at the same time as regulators are threatening to force banks to increase their capital requirements.

Robert Hormats, Vice Chairman of Goldman Sachs, is to be installed as Under Secretary of Economics, Business, and Agricultural Affairs. This comes as one more, probably unnecessary reminder of the total control exercised by Wall Street over the Obama administration’s economic and financial policy…he will find plenty of old friends used to making decisions, almost all of them uniformly disastrous for the U.S. and global economy…

Hormats’ agricultural responsibilities will of necessity bring him into frequent contact with the Chairman of the Commodity Futures Trading Commission, Gary Gensler – a former Goldman partner.

As Assistant Secretary of Treasury in the Clinton Adminsitration Gensler played a key role in greasing the skids for the notorious Commodity Futures Modernization Act of 2000, which set the stage for the great credit default swaps scam that underpinned the recent bubble and subsequent collapse. News of the appointment did generate threats of obstruction in the Senate – any one of the senators could have blocked the appointment had they really wished to do so – but such threats proved predictably hollow. Had they been otherwise, Treasury Chief of Staff Mark Patterson could of course have lent the expertise he gained as Goldman’s lobbyist to overcome the obstacle.

Such connection to the key enablers of our bankrupt casino helps explain many of the other hires listed above.

Some plans want to hide the truth from taxpayers

Public employee pension plans are plagued by overgenerous benefits, chronicunderfunding, and now trillion dollar stock-market losses. Based on their preferred accounting methods — which discount future liabilities based on high but uncertain returns projected for investments — these plans are underfunded nationally by around $310 billion.

The numbers are worse using market valuation methods (the methods private-sector plans must use), which discount benefit liabilities at lower interest rates to reflect the chance that the expected returns won’t be realized. Using that method, University of Chicago economists Robert Novy-Marx and Joshua Rauh calculate that, even prior to the market collapse, public pensions were actually short by nearly $2 trillion. That’s nearly $87,000 per plan participant. With employee benefits guaranteed by law and sometimes even by state constitutions, it’s likely these gargantuan shortfalls will have to be borne by unsuspecting taxpayers…

For these reasons, the Public Interest Committee of the American Academy of Actuaries recently stated, “it is in the public interest for retirement plans to disclose consistent measures of the economic value of plan assets and liabilities in order to provide the benefits promised by plan sponsors.”

Nevertheless, the National Association of State Retirement Administrators, an umbrella group representing government employee pension funds, effectively wants other public plans to take the same low road that the two Montana plans want to take. It argues against reporting the market valuation of pension shortfalls. But the association’s objections seem less against market valuation itself than against the fact that higher reported underfunding “could encourage public sector plan sponsors to abandon their traditional pension plans in lieu of defined contribution plans.”

Big Banks Don’t Want California’s IOUs A group of the biggest U.S. banks said they would stop accepting California’s IOUs on Friday, adding pressure on the state to close its $26.3 billion annual budget gap…The group of banks included Bank of America Corp., Citigroup Inc., Wells Fargo & Co. and J.P. Morgan Chase & Co., among others.

June saw officially 473,000 jobs lost in the non-farm sector. If you add in the bogus “birth/death” ratio of 185,000 jobs, 20,000 more than last June, you have a real number of 658,000 jobs lost. Now you can understand why U6 is not 16.5% and in reality is 20.5% unemployment.

The workweek was at a record low of 33 hours. Can you imagine how many people are working part-time? John Williams who is better at this than I am has it at 20.6%.

For further analysis by Bob Chapman visit:

www.TheInternationalForecaster.com