Japan has not only suffered from dismal macroeconomic performance over the past two decades, but it has lost its edge in areas of its greatest competitive strength, such as electronics, especially information and communications technology (ICT) hardware.Japanese electronics firms have declined by many standard measures of industrial performance, such as market share, exports, and profits.

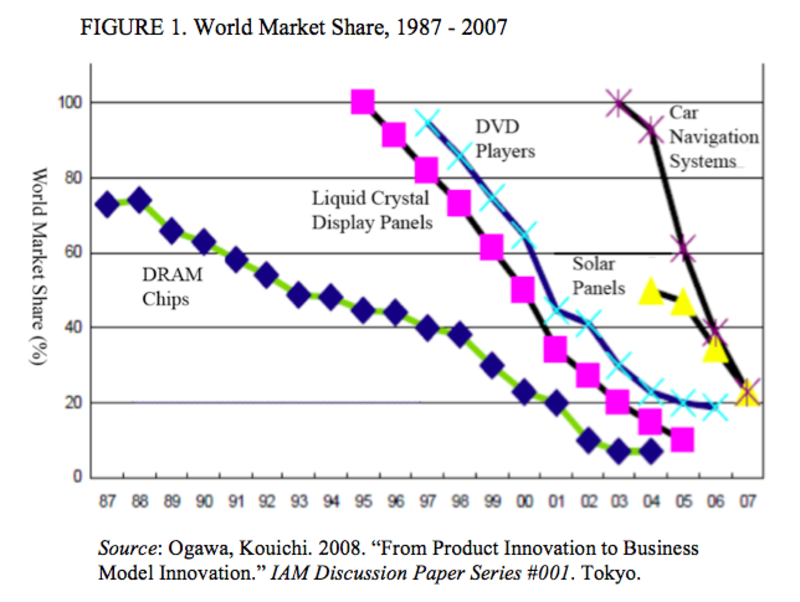

Japan’s postwar economic miracle did not quietly fizzle out, but rather exploded in grandiose fashion in the early 1990s. Japan’s descent from industrial dominance arrived later, evolved more slowly, and varied considerably by sector – and yet the turn of fortunes was equally stunning. Japanese manufacturers’ global market share dropped from 76 to 3 percent from 1987 to 2004 in DRAM chips; from 95 to 20 percent from 1997 to 2006 in DVD players; from 100 to 5 percent from 1995 to 2005 in liquid crystal display panels; from 100 to 20 percent from 2003 to 2007 in car navigation systems; from 45 to 21 percent from 2004 to 2007 in solar energy panels; and from 90 to 48 percent from 2000 to 2008 in lithium ion batteries (See Figure 1).2 One government report estimates that Japanese electronics companies produced 70 percent of an iPod in 2005 but only 20 percent of an iPad in 2010.3 Japan’s share of OECD ICT goods exports dropped from 16.8 percent in 1999 to 10.4 percent in 2011 (See Table 1).

|

JAPAN’S CHALLENGE

So what went wrong? In short, recent developments in the global economy have severely undermined Japanese firms’ institutional strengths and exacerbated their weaknesses. Japan’s weak macro-economic performance contributed to declining industrial competitiveness because it left the government and the private sector with diminished resources to invest toward future productivity gains.Beyond that, however, Japanese firms have confronted two critical challenges: the decomposition of production and the services transformation.The decomposition of production refers to the process whereby integral production centered in one country has given way to modular production and global supply chains.In the earlier era, vertically integrated manufacturers controlled the production process from research through production to final assembly.In the current period, manufacturers engage in more outsourcing, purchasing goods or services from outside the firm, and offshoring, moving production abroad or purchasing from a foreign supplier.The services transformation refers not only to the growth of services relative to manufacturing but also to the integration of manufacturing itself with more service functions, including software and applications.4

|

The decomposition of production has undermined the competitive advantage of Japanese business models that rely on long-term relationships with suppliers, banks, and workers to foster incremental advances in production processes.Japanese manufacturers have maintained a stronger competitive position in products that continue to be characterized by integral production (such as automobiles and digital cameras) than in those that have shifted further to modular production (such as personal computers and cellular telephones).5

The recent evolution of international competition is not one discrete change but rather a cluster of developments, and these developments have affected different subsectors and firms in distinct ways.For example, the decomposition of production has hit Japan’s integrated electronics manufacturers particularly hard.In the United States, the disintegration of the production chain drove the transformation of the electronics and information industries.U.S. antitrust policies broke up the supply chain, and regulatory reforms in finance and telecommunications fueled user-driven innovation.This heralded the “Wintelist” era (named for Microsoft Windows plus Intel), in which integrated electronics firms such as AT&T or IBM no longer controlled technological standards, but shared control with downstream suppliers, including software companies and semiconductor specialists.6 In the earlier period, Japan’s integrated electronics producers were seen to have an advantage over American merchant semiconductor manufacturers because their computer divisions could subsidize their semiconductor operations.7In the Internet age, however, this integration became a liability as Japanese electronics firms were slow to capture either the cost benefits of modular production or the innovative potential of independent software and components firms.8Some of the most successful U.S. firms have relied increasingly on foreign specialists such as Foxconn in China to handle manufacturing, focusing primarily on design and marketing.Japanese electronics companies have also shifted production of the more bulky and lower-tech electronic products, such as televisions, to China, but they have maintained greater control over manufacturing relative to their U.S. counterparts.Some Japanese firms have sold facilities to manufacturing service companies, but they have done so more as a means of cutting costs than as a strategic reorganization of the production process.9

Moreover, the services transformation has tested Japanese manufacturers because it relies on capabilities in areas of their weakness – such as services, software, entertainment, and system integration – or on ties with firms that possess those capabilities.Observers have characterized Japan as having a “dual economy,” comprised of an internationally competitive sector focused in manufacturing and a domestic protected sector centered in services.And this dual economy has been characterized by a particularly wide gap in productivity between the two sectors.10 Hence a shift in the locus of growth in the global economy from manufacturing to services and toward greater integration of manufacturing and services implies a shift away from Japan’s comparative advantage.

The services transformation also involves the use of advanced software embedded in manufacturing, and yet Japan lags in many areas of software development.11 Arora, Branstetter, and Drev contend that this shift is the single most important factor in Japan’s competitive decline in the IT sector relative to the United States.They find that U.S. firms improved their relative performance over the course of the 1990s but advanced most dramatically in those areas where software competence was most critical.Moreover, IT patents granted by the U.S. government – including hardware patents – increasingly cite software technology, yet Japanese firms were less likely to cite software than their competitors, suggesting that their innovations were less reliant on advances in software.12

Japanese firms’ strong orientation toward the domestic market rather than the global marketplace has hindered their ability to take advantage of both the decomposition of production and the services transformation.Commentators now commonly refer to this as the “Galapagos” phenomenon.That is, Japanese manufacturers develop high-quality products that are only suited for the Japanese market.13 In a classic example, Japanese electronics companies produce some of the most sophisticated cellular telephones in the world, and they dominate the Japanese market,and yet they have not succeeded in world markets because the handsets are not suited to global technical standards, their features are tailored to Japanese tastes, and their prices are too high.

Japanese firms have a strong record of innovation, but they have a greater capacity for incremental improvements in production processes than in breakthrough discoveries.This balance of strength and weaknesses reflects Japan’s comparative institutional advantages.In some sectors, however, breakthrough innovations have become more important in recent years while production improvements are less so.In the semiconductor industry, for example, U.S. makers have had the edge in innovation and Japanese producers have excelled in production – but the production advantage was more decisive in the lean production era while the innovation advantage is more critical today, due primarily to more rapid product cycles.In the 1970s and 1980s, U.S. firms could not keep up with Japanese rivals that emulated their technology and achieved better quality, higher volume, and lower costs in production.Now U.S. companies prevail because the innovation cycle has accelerated and designs have become more complex.14 Japanese firms continue to perform well in terms of patents overall, but they lag considerably in the fasting-growing sectors, such as software and information technology.

Japan also has a disadvantage in the current era because it has relatively little new entry into the market.This means that Japanese firms have adjusted to new developments via incremental reform by existing companies rather than radical innovation by new companies.In the United States, some incumbent firms have struggled to adapt to the new environment, just like their Japanese counterparts.Meanwhile, firms with radically new business models, such as Apple and Google, have emerged as market leaders.

JAPAN’S GOVERNANCE PROBLEM

If Japanese corporations have not revamped their strategies sufficiently to adapt to the information age, then why hasn’t the government been able to do more to transform the institutional context and to promote private sector reform?In the past, the government played the leading role in reshaping Japan’s market structure.So why not now?

The Japanese government has responded to declining industrial competitiveness with incremental adjustments, not bold reform.In some sense, the government’s caution is warranted.The government has sought to give corporations more flexibility to restructure while preserving the strengths of the Japanese model, including stable employment relations and coordination among firms.Moreover, the government’s approach has reflected the preferences of the Japanese people, who have been wary of reforms that would deliver higher financial returns at the expense of greater risks.Thus the government’s reluctance to deliver bold liberal market reforms reflects the normal functioning of the political system and not its failure.15

Nonetheless, the Japanese government’s policy record reveals some troubling weaknesses, particularly when it comes to the information technology sector.By abandoning its own state-led model and yet not adopting a liberal market model either, the government has risked undermining Japan’s comparative institutional advantages without cultivating a viable alternative.

It is tempting to blame Japan’s incoherent economic strategy on the pervasive political instability since the LDP first lost power in 1993.The unwieldy coalition that replaced the LDP lasted less than a year, giving way to a series of LDP-led coalition governments, frequent realignment among the opposition parties, and a long series of forgettable prime ministers.Prime Minister Koizumi Junichiro was the notable exception during this period, yet even he did not substantially alter the trajectory of economic reform beyond postal privatization and the banking clean-up.Some of the signature Koizumi structural reforms, such as the reform of the special public corporations, were well under way before Koizumi took office.And on many other issues, such as labor policy or corporate governance reform, the bureaucracy simply continued on a path of incremental adjustments.

Prime Minister Abe Shinzo had stressed innovation as a major theme during his first term (2006-07), but he did not stay in office long enough to make substantial progress.When he returned as prime minister in December 2012, he placed economic reform as his top priority, proposing three “arrows” for reform: aggressive monetary easing, fiscal stimulus, and structural reform.The first two arrows contributed to an economic upturn in 2013, but many analysts concluded that longer-term growth prospects hinged on the third arrow.Government proposals for structural reform gave substantial attention to the IT sector, proposing a reorganization and strengthening of government support for R&D, strengthening the IT infrastructure, and promoting IT usage in government, schools, and society at large.16

Yet Japan’s postwar political system has rarely been characterized by strong political leadership on economic policy issues.Thus I would contend that Japan’s lack of a coherent economic strategy since 1990 reflects a decline in bureaucratic leadership more than political volatility.The core economic ministries, particularly METI and MOF, have experienced a profound loss of prestige, confidence, and power.The government officials themselves have lost faith in the government’s ability to enhance Japan’s competitiveness.Meanwhile, politicians have made bureaucrat-bashing a major theme in their political strategies.This shifts the blame for economic problems from politicians to bureaucrats, it appeals to popular disillusionment with the bureaucracy, and it gives divided political parties an issue to unite them.

Even if Japan could resolve its governance problem, that leaves us with a big question: What exactly should the Japanese government be doing to support the revival of Japanese electronics?Some would argue that it should move decisively in the direction of the “liberal market” model of the United States.The new global economy rewards countries with low barriers to entry, fluid labor markets, open technical standards, modular production integrated into global supply chains, and robust competition in product markets, telecommunications, and financial services.

Others would propose precisely the opposite: Japan must preserve its own institutional strengths.Japan could still leverage its capable bureaucracy, strong government-industry ties, and close collaboration among firms, suppliers, banks, and workers as sources of competitive advantage.In fact, Japan has underemployed its advantages and allowed some to atrophy.

I would argue that both of these perspectives bear some truth, and therefore the Japanese government was right to combine market liberalization with selective efforts at state-led industrial policy and government-industry coordination.But it delivered the wrong mix.It proceeded too slowly with pro-competitive reform where it was most needed, such as in telecommunications regulation, and too tentatively with state support where it was most appropriate, such as in supporting R&D and promoting IT diffusion.After all, Japan’s most successful rival, South Korea, has also deployed a combined strategy, with greater success.

South Korea and Japan began in similar positions in 1990s, albeit with Japan holding a clear technological lead in most high-technology sectors.South Korea and Japan had both succeeded in the postwar era with a state-led growth strategy combined with strong government-industry ties and a highly organized private sector.And yet in recent years South Korea has been gaining market share in electronics and many ICT sectors while Japan has been losing share.The South Korean government has been more aggressive than the Japanese government with market reforms since the Asian crisis of 1997.It moved sooner than Japan to promote competition in telecommunications and support IT diffusion.It aggressively pursued bilateral free trade and investment packages.It encouraged Korean industry to adjust to international technical standards.Meanwhile, the Korean government has provided stronger support for business R&D and investment, and it has pressed more aggressively for coordination and consolidation in key sectors. Overall both the Japanese and South Korean governments have opted for a mixed strategy: neither fully adhering to the old state-led model nor dramatically switching to a neo-liberal one.Yet the South Korean government and corporations have crafted a more effective mix.

Steven K. Vogel is Professor of Political Science at the University of California, Berkeley. He specializes in the political economy of the advanced industrialized nations, especially Japan. He is the author of Japan Remodeled: How Government and Industry Are Reforming Japanese Capitalism (Cornell, 2006) and co-editor (with Naazneen Barma) of The Political Economy Reader: Markets as Institutions (Routledge, 2007). His earlier book, Freer Markets, More Rules: Regulatory Reform in Advanced Industrial Countries (Cornell University Press, 1996), won the 1998 Masayoshi Ohira Memorial Prize. He has also edited a volume entitled U.S. – Japan Relations in a Changing World (Brookings Institution Press, 2002).

Related Articles

• Abe, Big Data and Bad Dreams: Japan’s ICT Future?

• Jenny Chan, Ngai Pun and Mark Selden, The politics of global production: Apple, Foxconn and China’s new working class

• Andrew DeWit, Japan: Building a Galapagos of Power?

• R. Taggart Murphy, Assessing the Economic Aftershocks of Japan’s March 11 Earthquake

• R. Taggart Murphy, Japan As Number One in the Global Economic Crisis: Lessons for the World

Notes

1 This article is based on Steven K. Vogel, “Japan’s Information Technology Challenge,” in Dan Breznitz and John Zysman, The Third Globalization: Can Wealthy Nations Stay Rich in the Twenty-First Century? (Oxford: Oxford University Press, 2013), 350-72.

2 METI, “Jouhou keizai kakushin senryaku (gaiyou)” [Information Economy Renovation Strategy (Summary)] (May 2010), 3; METI, “Sangyou kouzou,” 22.

3 METI, “Jouhou keizai,” 4.

4 Breznitz and Zysman, The Third Globalization, 4-12.

5 METI, “Sangyou kouzou bijon gaiyou” [Industrial Structure Vision Outline] (June 2010), 24.

6 Abraham Newman and John Zysman, “Transforming Politics in the Digital Era,” in Zysman and Newman, eds., How Revolutionary Was the Digital Revolution? National Responses, Market Transitions, and Global Technology (Stanford: Stanford Business Books, 2006), 391-411.

7 Michael G. Borrus, Competing for Control: America’s Stake in Microelectronics (Cambridge, MA: Ballinger, 1988).

8 Robert E. Cole and D. Hugh Whittaker, “Introduction,” in Whittaker and Cole, eds., Recovering From Success: Innovation and Technology Management in Japan (Oxford: Oxford University Press, 2006), 8-14.

9 METI, “Jouhou keizai,” 8.

10 Richard Katz, Japan The System That Soured: The Rise and Fall of the Japanese Economic Miracle (Armonk, NY: M.E. Sharpe, 1998), 29-46

11 Robert E. Cole, “Software’s Hidden Challenges,” in Whittaker and Cole, eds., Recovering From Success: Innovation and Technology Management in Japan (Oxford: Oxford University Press, 2006), 105-26; Robert E. Cole and Shinya Fushimi, “The Japanese Enterprise Software Industry: An Evolutionary and Comparative Perspective,” in Hiroaki Miyoshi and Yoshifumi Nakata, eds., Have Japanese Firms Changed? The Lost Decade (Houndmills, Basingstoke, Hampshire, UK: Palgrave MacMillan, 2011), 41-69

12 Ashish Arora, Lee G. Branstetter, and Matej Drev, “Going Soft: How the Rise of Software-Based Innovation Led to the Decline of Japan’s IT Industry and the Resurgence of Silicon Valley,” National Bureau of Economic Research Working Paper 16156 (July 2010).

13 Kenji E. Kushida, “Leading Without Followers: How Politics and Market Dynamics Trapped Innovations in Japan’s Domestic ‘Galapagos’ Telecommunications Sector,” Journal of Industry, Competition, and Trade (2011) 11: 279-307.

14 Steven K. Vogel and John Zysman, “Technology,” in Vogel, ed., U.S.-Japan Relations in a Changing World (Washington D.C.: Brookings Institution Press, 2002), 252.

15 Vogel, Japan Remodeled, 44-45, 51-61.

16 “Nihon saikou senryaku – Japan is Back” [Japan Revitalization Strategy], June 14, 2013.

– See more at: http://japanfocus.org/-Steven_K_-Vogel/4026#sthash.768J3KnW.dpuf