Obama’s Financial Crimes Enforcement Network Protects Bank Fraud and Insider Trading

Obama's New SEC 'Sheriff.' No Conflict of Interest When it Comes to Shielding Wall Street's Pin Striped Mafia

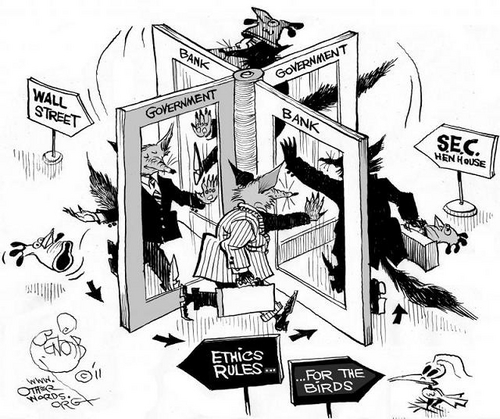

One indelible sign of state capture by pirate corporations and the financial jackals holding sway on Wall Street and the City of London is the ease with which former “regulators” slip into plum positions with the firms whom they supposedly “regulated” as “public servants.”

While the drone kill-crazy Obama regime has done yeoman’s work cementing in place extra-constitutional policies first enacted by the Bush gang–only to exceed Bushist depredations by a whole order of magnitude–kool-aid sipping “progressives” and troglodytic “conservatives” have given the president a free pass when it comes to policing the financial criminals who blew up the world economy.

But when it comes to US spy agencies probing and sweeping up your financial information, well, the sky’s the limit!

As Reuters reported last week, the administration “is drawing up plans” to give securocrats “full access to a massive database that contains financial data on American citizens and others who bank in the country, according to a Treasury Department document.”

That Treasury plan would give secret state apparatchiks, including those ensconced at CIA, NSA and the Pentagon free reign to rummage through the Financial Crimes Enforcement Network’s (FinCEN) massive database of “suspicious activity reports” routinely filed by “banks, securities dealers, casinos and money and wire transfer agencies.” The FBI and DHS already have full access to that database under the Orwellian USA Patriot Act.

Under the proposal, FinCen data will be linked “with a computer network used by US defense and law enforcement agencies to share classified information called the Joint Worldwide Intelligence Communications System,” according to Reuters.

And since requirements for filing SARs are “so strict,” banks often “over-report,” this “raises the possibility that the financial details of ordinary citizens could wind up in the hands of spy agencies,” where it will live in perpetuity, “criminal evidence, ready for use in a trial,” as Cryptohippie famously warned.

Got that? While Wall Street drug banks are handled with care because of the “collateral consequences” that might result from a criminal referral for laundering billions of narco-dollars, the average citizen’s financial data will be fair game.

Which brings us back to Obama’s anemic regulatory regime and the “sheriffs” eager to do the bankster’s bidding.

Wall Street’s Choice

As one of the filthiest dens of corruption in Washington, the Securities and Exchange Commission (SEC) is in a league of its own.

In late January, when the president announced he was nominating former federal prosecutor Mary Jo White to lead the Securities and Exchange Commission (SEC), The New York Times, as they are wont to do, proclaimed that the “White House delivered a strong message to Wall Street.”

A rather ironic assertion considering the tens of millions of dollars “earned” defending Wall Street criminals by Debevoise & Plimpton partner Mary Jo and her millionaire lawyer husband John, a partner at the white shoe corporate litigation shop Cravath, Swaine & Moore, as Above the Law disclosed.

Keep in mind that White will soon lead an agency that for years covered-up financial crimes by routinely shredding tens of thousands of case files on everything from insider trading, securities fraud, market manipulation and the Madoff and Stanford Ponzi schemes, as a 2011 Rolling Stone investigation disclosed.

As I reported nearly three years ago during my investigation into now-convicted fraudster Allen Stanford’s ties to the CIA over his role in laundering oceans of cash for the Agency’s narcotrafficking assets, the SEC’s Fort Worth office “stood down” multiple probes “at the request of another federal agency,” which regional head of enforcement Stephen J. Korotash “declined to name.”

Indeed, a 2010 report by the SEC’s Office of the Inspector General found that another “former head of Enforcement in Fort Worth,” Spencer C. Barasch, “played a significant role in multiple decisions over the years to quash investigations of Stanford,” and sought to represent the dodgy banker “on three separate occasions after he left the Commission, and in fact represented Stanford briefly in 2006 before he was informed by the SEC Ethics Office that it was improper to do so.”

Barasch eventually paid a $50,000 fine for ethics violations and “moved on.”

Despite the SEC’s documented history of sleaze and lax enforcement of rules that would earn the average citizen a one-way ticket to the slammer, on March 19 the Senate Banking Committee approved White’s nomination by a vote of 21-1; the lone dissenter was Sherrod Brown (D-OH). A vote by the full Senate could come as early as next week and she is expected to be confirmed easily.

As a former US Attorney for the Southern District in New York (1993-2002), White has been described by corporate media as a “tough as nails” prosecutor for her role in bringing down Mafia wise guy John Gotti and for running to ground criminal mastermind Ramzi Yousef, the architect of the 1993 World Trade Center bombing. (For a gripping account of how the FBI and US prosecutor’s office botched that investigation and “foamed the runway” for the mass murder of 3,000 people on 9/11, readers should train their sights on Peter Lance’s exposé, 1000 Years for Revenge).

White’s record when it came to holding financial criminals to account however, was even more dubious; in fact, for more than a decade she’s defended them.

Times’ stenographers dialed back their glowing encomiums for the Obama nominee, writing that “translating that message into action will not be easy, given the complexities of the market and Wall Street’s aggressive nature.”

As reliable hands on the financial beat, Dealbook reporters routinely trumpet everything from the Justice Department’s sweetheart deal with drug money laundering and terrorist coddling banking giant HSBC to kissing Jamie Dimon’s hem over billions of JPMorgan Chase losses last year in what were euphemistically described as a “bad bet on derivatives.”

In the January puff-piece, reporters Ben Protess and Benjamin Weiser outdid themselves, claiming that with the White nomination “the president showed a renewed resolve to hold Wall Street accountable for wrongdoing.”

However, a less than laudatory piece published by Bloomberg News took those fatuous claims to task. Financial columnist Jonathan Weil observed that while “The Securities and Exchange Commission couldn’t get Ken Lewis on any securities-law violations after he helped drive Bank of America Corp. into the ground as its chief executive officer,” the agency “is poised to get his attorney as its new chairman–and Morgan Stanley’s, too.”

But hey, it’s not like the SEC is chock-a-block with conflicts of interest, right? Well, if a bracing read is what the doctor ordered, then turn your attention to a damning study released last month by the Project on Government Oversight (POGO). Entitled, Dangerous Liaisons: Revolving Door at SEC Creates Risk of Regulatory Capture, author Michael Smallberg takes us on a 60-page tour of insider dealing and corruption that would make a Roman emperor blush.

According to Smallberg: “Between 2001 and 2010, more than 400 SEC alumni filed nearly 2,000 disclosure statements saying they planned to represent employers or clients before the agency. These alumni have represented companies during SEC investigations, lobbied the agency on proposed regulations, obtained waivers to soften the blow of enforcement actions, and helped clients win exemptions from federal law. On the other side of the revolving door, when industry veterans join the SEC, they may be in a position to oversee their former employers or clients, or may be forced to recuse themselves from working on crucial agency issues.”

Talk about an agency blind in both eyes by design!

A Counsel with ‘Juice’

One of the more egregious cases which came to light was SEC’s handling of a 2005 insider trading case involving former agency enforcement head, Linda Thomsen, White and her client, Morgan Stanley CEO John Mack.

Before her tenure as the agency’s chief enforcement officer, Thomsen was in private practice at the powerhouse New York law firm, Davis, Polk & Wardell. During the capitalist financial meltdown, the company represented upstanding corporate citizens such as AIG, Freddie Mack, Lehman Brothers and drug-tainted Citigroup. Bulking up a stable of attorneys well-versed in regulatory matters, the firm has hired other former SEC officials, including Commissioner Annette Nazareth and Linda Thomsen.

Before sailing off to greener shores at Davis, Polk, Nazareth’s claim to fame was standing up a voluntary “supervisory regime” for the largest “investment bank holding companies” who “policed” themselves by cratering the economy and costing taxpayers trillions in bailouts.

That program, the Consolidated Supervised Entity was scrapped in 2008. Why? According to a press release by then SEC head Christopher Cox (no slouch himself when it came to defending his corporatist masters): “The last six months have made it abundantly clear that voluntary regulation does not work. When Congress passed the Gramm-Leach-Bliley Act, it created a significant regulatory gap by failing to give to the SEC or any agency the authority to regulate large investment bank holding companies, like Goldman Sachs, Morgan Stanley, Merrill Lynch, Lehman Brothers, and Bear Stearns.” (emphasis added)

A “gap” large enough to fly a fleet 747s through and still have enough wiggle room to launch a dozen Saturn 5s into deep space!

And that insider trading case?

According to Matt Taibbi’s Rolling Stone investigation, in September 2004 SEC investigator Gary Aguirre was tasked to look into an insider trading complaint against “a hedge-fund megastar named Art Samberg. One day, with no advance research or discussion, Samberg had suddenly started buying up huge quantities of shares in a firm called Heller Financial.”

Samberg was the founder of the multibillion dollar hedge fund, Pequot Capital Management, a firm which invested in a multitude of private and public equities and what are known as “distressed securities.” These are investment instruments held by firms or government entities (paging Fannie Mae!) that are either in default, under bankruptcy protection or will soon be heading south. The most common securities of this type are bonds and bank debt (think residential mortgage backed securities and other toxic assets). Since the financial crisis, a booming market in distressed securities have earned savvy hedge fund mangers billions in fees as they seek influence with regulators over how that debt is restructured.

And since “influence” in Washington and the “juice” that comes with it on Wall Street is the name of the game, well, you get the picture.

“‘It was as if Art Samberg woke up one morning and a voice from the heavens told him to start buying Heller,’ Aguirre recalls. ‘And he wasn’t just buying shares–there were some days when he was trying to buy three times as many shares as were being traded that day.’ A few weeks later, Heller was bought by General Electric–and Samberg pocketed $18 million.”

“After some digging,” Taibbi wrote, “Aguirre found himself focusing on one suspect as the likely source who had tipped Samberg off: John Mack, a close friend of Samberg’s who had just stepped down as president of Morgan Stanley.”

According to Taibbi, “Mack flew to Switzerland to interview for a top job at Credit Suisse First Boston. Among the investment bank’s clients, as it happened, was a firm called Heller Financial. We don’t know for sure what Mack learned on his Swiss trip; years later, Mack would claim that he had thrown away his notes about the meetings.”

Rather conveniently, one might say.

In any event after returning from his Swiss Alps sojourn, in a classic case of “you scratch my back” Samberg cut his buddy Mack into a deal with a tech firm called Lucent, “a favor that netted him [Mack] more than $10 million.” Shortly thereafter, “Samberg began buying-up every Heller share in sight, right before it was snapped up by GE.”

An insider trading case worthy of further scrutiny, right? But when Aguirre told his boss [Robert Hanson] that he intended to interview Mack and the other principals, “things started getting weird.” Taibbi noted that Aguirre’s boss told the investigator that Mack “had powerful political connections.”

Indeed he did. Like other Wall Street banksters, Mack had been a fundraising “Ranger” for the 2004 George W. Bush campaign, and when it became clear that a new product line needed to be rolled out, Mack crossed party lines and backed Hillary Clinton’s ill-starred 2008 bid for the Oval Office.

How’s that for clubby “bipartisanship”!

A 2007 report (large PDF file) published by the Senate Finance Committee titled The Firing of an SEC Attorney and the Investigation of Pequot Management, disclosed that “at least three experienced SEC officials believed in the summer of 2005 that questioning John Mack was an appropriate next step in the Pequot Investigation.”

Indeed, Senate investigators revealed that “the most significant aspect” of Mack’s 2006 SEC testimony (after the statute of limitations for prosecution had expired) “is his acknowledgement that he went to Switzerland to discuss becoming CSFB’s CEO from July 26-28, 2001.”

“In view of the fact that Mack also spoke with Samberg immediately upon his return to the United States on July 29, 2001,” Senate staff disclosed, “the trading day before Samberg began heavily betting on Heller Financial stock, and on the same night Mack was permitted into a lucrative deal, there was more than a sufficient basis to justify taking Mack’s testimony in the summer of 2005.”

After first being given the go-ahead to interview Mack, “Aguirre’s direct line of supervisors” including Hanson, Mark Kreitman and Paul Berger, got cold feet. Unfortunately for Aguirre, this came after he had briefed attorneys at Mary Jo White’s old stomping ground and “criminal authorities in the Southern District opened their own investigations” into dubious deals between Samberg and Mack.

At that point, Senate investigators averred, “his supervisors’ attitudes shifted dramatically,” that is, “when officials from Morgan Stanley began contacting the SEC to learn about the potential impact of the investigation on its prospective CEO, John Mack.” Only then did Hanson warn Aguirre that “it would be difficult to subpoena John Mack because of his ‘powerful political connections’.”

Aguirre told Senate investigators that “in a face-to-face meeting” with his boss, “Hanson said it would be very difficult to get permission to question Mack because of Mack’s ‘powerful political connections’.”

Hanson however, denied everything and said during his Senate testimony “That doesn’t sound like something I would say.”

“As a general matter,” Hanson testified, “I try to alert folk above me about significant developments in investigations that may trigger calls and the like so that they are not caught flat footed. I also think that Paul [Berger] and Linda [Thomsen] would want to know if and when we are planning to take Mack’s testimony so that they can anticipate the response, which may include press calls that will likely follow. Mack’s counsel will have ‘juice’ as I described last night–meaning that they will reach out to Paul and Linda (and possibly others).”

And who was Mack’s “juiced” attorney? Why none other than Mary Jo White!

Unbeknownst to Aguirre, his supervisors were trading emails about his imminent firing from the agency. “With no knowledge of those emails,” Senate investigators disclosed that Aguirre wrote Hanson again stating, that “before and after the Mack decision, you have told [me] several times that the problem in taking Mack’s exam is his political clout, e.g., all the people that Mary Jo White can contact with a phone call.”

At the same time that Aguirre was seeking to subpoena Mack’s testimony, Morgan Stanley’s board hired Debevoise & Plimpton to vet their soon-to-be reinstalled CEO. “Only two days after being retained,” the Senate reported, “White did what the SEC did not do until more than a year later. She questioned John Mack: ‘The other thing that I did for the board to gather what information I could on that time frame was to interview John Mack himself,'” White told investigators.

But she did more than that, demonstrating she indeed had plenty of “juice.”

“That evening,” the Senate disclosed, “White sent Thomsen an e-mail message marked ‘URGENT’ and asked that Thomsen return the call ‘this evening.’ Aguirre complained that the next day White delivered the e-mails that he had subpoenaed from Morgan Stanley directly to Linda Thomsen.”

“On June 27,” Aguirre testified, “I learned that Mack-Samberg emails, which I had subpoenaed from Morgan Stanley, had been delivered directly to the Director of Enforcement, Linda Thomsen. Neither I nor other staff had heard of this happening before. Indeed, the subpoena explicitly stated that the documents were to be delivered to me.”

Evidence reviewed by the Senate Finance Committee “suggests that the reluctance to question Mack represents a much more subtle and pervasive problem than an individual partisan political favor. SEC officials were overly deferential to Mack–not because of his politics–but because he was an ‘industry captain’ who could hire influential counsel to represent him.”

“In a shocking move that was later singled out by Senate investigators,” Taibbi wrote, “the director actually appeared to reassure White, dismissing the case against Mack as ‘smoke’ rather than ‘fire’.”

“Aguirre didn’t stand a chance,” Taibbi noted. “A month after he complained to his supervisors that he was being blocked from interviewing Mack, he was summarily fired, without notice. The case against Mack was immediately dropped: all depositions canceled, no further subpoenas issued. ‘It all happened so fast, I needed a seat belt,’ recalls Aguirre, who had just received a stellar performance review from his bosses. The SEC eventually paid Aguirre a settlement of $755,000 for wrongful dismissal.”

It gets better.

In a subsequent piece, Taibbi followed-up and discovered “not only did the SEC ultimately delay the interview of Mack until after the statute of limitations had expired, and not only did the agency demand an investigation into possible alternative sources for Samberg’s tip (what Aguirre jokes was like ‘O.J.’s search for the real killers’), but the SEC official who had quashed the Mack investigation, Paul Berger, took a lucrative job working for Morgan Stanley’s law firm, Debevoise and Plimpton, just nine months after Aguirre was fired.”

As it turned out, at the exact moment that Aguirre’s investigation was being sabotaged, Senate investigators “uncovered an email to Berger from another SEC official, Lawrence West, who was also interviewing with Debevoise and Plimpton at the time.”

“The e-mail was dated September 8, 2005 and addressed to Paul Berger with the subject line, ‘Debevoise.’ The body of the message read, ‘Mary Jo [White] just called. I mentioned your interest’.”

Taibbi observed: “So Berger was passing notes in class to Mary Jo White about wanting to work for Morgan Stanley’s law firm while he was in the middle of quashing an investigation into a major insider trading case involving the CEO of the bank. After the case dies, Berger later gets the multimillion-dollar posting and the circle is closed.”

In later testimony to the Inspector General into Debevoise & Plimpton’s eventual hiring of Berger by a firm that boasts on their web site that she leads a “team” which “includes eleven former Assistant US Attorneys,” White’s comments on whether Berger was considered too “aggressive” in prosecuting Wall Street criminals is all-too-revealing.

“You always have a spectrum on the aggressiveness scale for government types and was this an issue that was beyond real commitment to the job and the mission and bringing cases,” White affirmed, “which is a positive thing in the government, to a point. Or was it a broader issue that could leave resentment in the business community or in the legal community that would hamper his ability to function well in the private sector?”

“It’s certainly strange that White has to qualify the idea that bringing cases is a positive thing in a government official–that bringing cases is a ‘positive thing . . . to a point’,” Taibbi noted. “Can anyone imagine the future head of the DEA saying something like, ‘For a prosecutor, bringing drug cases is a positive, to a point’?”

And what about Linda Thomsen? In 2008, the SEC’s inspector general, H. David Kotz, urged disciplinary action against her over her role in Aguirre’s squashed investigation of Samberg and Mack. While Samberg was eventually forced out of business, barred from working as an investment adviser and paid a $28 million fine for his shenanigans, Thomsen landed on her feet.

After refusing to answer relevant questions in 2009 before the House Committee on Financial Services probe into the SEC’s failure to investigate the Bernie Madoff Ponzi scheme, due to a “collective desire to preserve the integrity of the investigative and prosecution processes” mind you, Thomsen resigned and rejoined Davis, Polk and Wardell.

Later that year, Kotz released a report to Congress of the IG’s investigation into a “Senior Officer” who provided “inside information” to a “former official.” As it turns out that “Senior Officer” was Linda Thomsen and that “official” was her former boss Stephen Cutler who had jumped ship and joined JPMorgan Chase.

According to The New York Times, “Kotz said his office has concluded its well-publicized investigation into whether the SEC’s enforcement director, Linda Chatman Thomsen, inappropriately provided inside information to her former boss, Stephen Cutler, now the general counsel of JPMorgan Chase, amid the bank’s negotiations to buy Bear Stearns in March 2008.”

“The inquiry,” the Times reported, “which began in response to an anonymous tip, confirmed that Mr. Cutler sought assurances from Ms. Thomsen before the takeover that JPMorgan would not be sued for prior actions by Bear Stearns.”

And who was representing JPMorgan Chase in the wake of the Bear Stearns collapse? If you guessed Mary Jo White, you’d be right again.

Less than three years later, during Senate Banking Committee confirmation hearings, White told the panel that “the American people will be my client, and I will work as zealously as possible on behalf of them.”

But when questioned by Sherrod Brown (D-OH) whether or not White agreed with US Attorney General Eric Holder’s statement which affirmed that “federal prosecutors are instructed . . . to look at . . . collateral consequences” should a financial institution or its officers be criminally charged, White agreed.

In a follow-up question, Brown wondered whether there is “a two-tiered system where we exempt the biggest banks because they have the most employees and shareholders who could be affected by criminal prosecution?”

White’s answer pretty much sums up everything that’s bent about Washington’s culture of impunity when it comes to the Wall Street crimes: “It’s a factor that prosecutors are directed to consider.”

“I do think the deferred prosecution instrument,” White asserted, “has been used a great deal on a number of companies, [and] was designed to be tough in terms of monetary sanctions, monitors–everything but the charge itself that might cause what the prosecutor might consider to be negative and undesirable collateral consequences to the public interest.”

But what about harsher sanctions such as stripped assets, handcuffs and a jail cell for drug money laundering and securities scamming banksters, punishments that might actually deter corporate crime?

Forgetaboutit!

Tom Burghardt is a researcher and activist based in the San Francisco Bay Area. In addition to publishing in Covert Action Quarterly and Global Research, he is a Contributing Editor with Cyrano’s Journal Today. His articles can be read on Dissident Voice, Pacific Free Press, Uncommon Thought Journal, and the whistleblowing website WikiLeaks. He is the editor of Police State America: U.S. Military “Civil Disturbance” Planning, distributed by AK Press and has contributed to the new book from Global Research, The Global Economic Crisis: The Great Depression of the XXI Century.